UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

SCHEDULE l4A

Proxy Statement Pursuant to Section 14(a) of

the Securities Exchange Act of 1934

Filed by the Registrant x

Filed by a Party other than the Registrant ¨

Check the appropriate box:

| ¨ | Preliminary Proxy Statement |

| ¨ | Confidential, for Use of the Commission Only (as permitted by Rule 14a-6(e)(2)) |

| x | Definitive Proxy Statement |

| ¨ | Definitive Additional Materials |

| ¨ | Soliciting Material Under § 240. l4a-l2 |

TEXAS PACIFIC LAND CORPORATION

(Name of Registrant As Specified In Its Charter)

| N/A |

| (Name of Person(s) Filing Proxy statement, if Other Than the Registrant) |

Payment of Filing Fee (Check the appropriate box):

| x | No fee required |

| ¨ | Fee paid previously with preliminary materials. |

| ¨ | Fee computed on table in exhibit required by Item 25(b) per Exchange Act Rules 14a-6(i)(1) and 0-11 |

TEXAS PACIFIC LAND CORPORATION

NOTICE OF ANNUAL MEETING OF STOCKHOLDERS

To Be Held on November 16, 2022

Dear Fellow Stockholders:

We invite you to attend the 2022 Annual Meeting of Stockholders of Texas Pacific Land Corporation, a Delaware corporation (the “Company”), which will be held on November 16, 2022, at 10:30 a.m. Central time (the “Annual Meeting”) at the Renaissance Dallas Hotel, 2222 North Stemmons Freeway, Dallas, Texas 75207. At the Annual Meeting, you will be asked to vote on the following proposals (as more fully described in the proxy statement accompanying this notice):

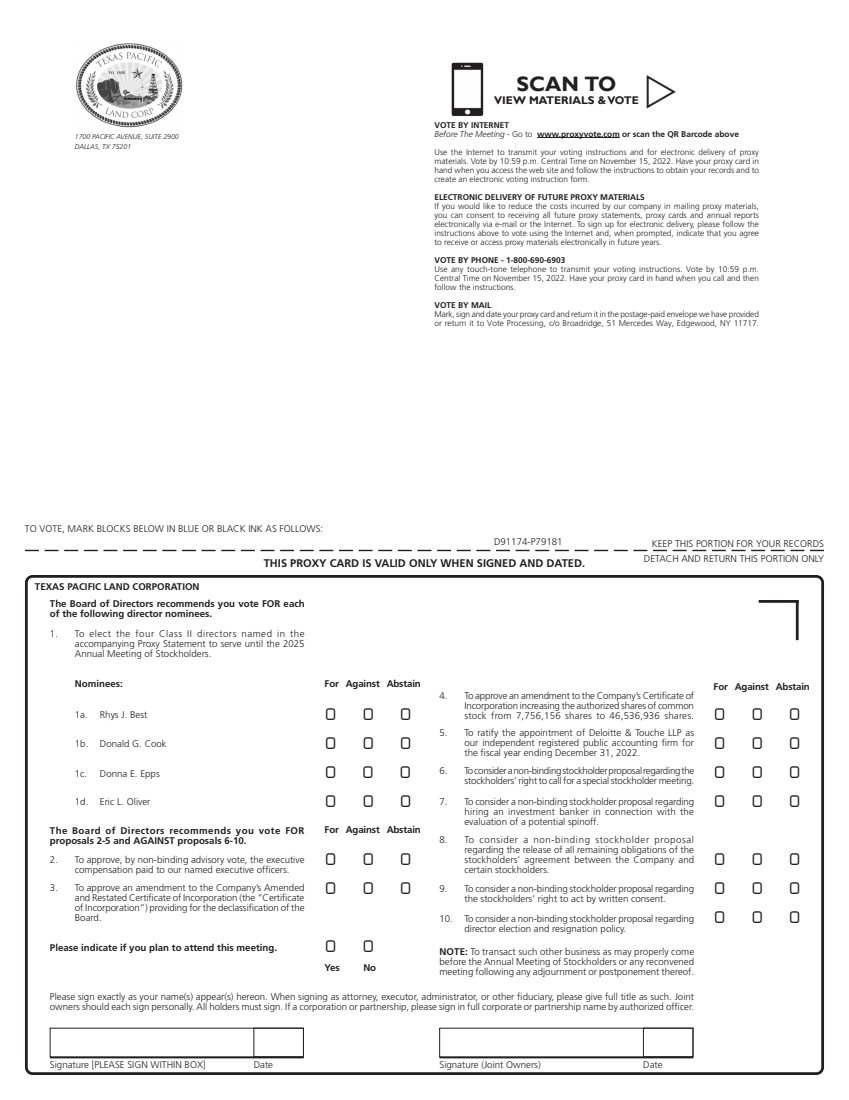

| 1. | To elect four (4) members of the Company’s Board of Directors (the “Board”) to serve until the 2025 Annual Meeting of Stockholders. |

| 2. | To approve, by non-binding advisory vote, the executive compensation paid to our named executive officers. |

| 3. | To approve an amendment to the Company’s Amended and Restated Certificate of Incorporation (the “Certificate of Incorporation”) providing for the declassification of the Board. |

| 4. | To approve an amendment to the Company’s Certificate of Incorporation increasing the authorized shares of common stock from 7,756,156 shares to 46,536,936 shares. |

| 5. | To ratify the appointment of Deloitte & Touche LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2022. |

| 6. | To consider a non-binding stockholder proposal regarding the stockholders’ right to call for a special stockholder meeting. |

| 7. | To consider a non-binding stockholder proposal regarding hiring an investment banker in connection with the evaluation of a potential spinoff. |

| 8. | To consider a non-binding stockholder proposal regarding the release of all remaining obligations of the stockholders’ agreement between the Company and certain stockholders. |

| 9. | To consider a non-binding stockholder proposal regarding the stockholders’ right to act by written consent. |

| 10. | To consider a non-binding stockholder proposal regarding director election and resignation policy. |

| 11. | To transact such other business as may properly come before the Annual Meeting or any adjournment thereof. |

Only stockholders of record at the close of business on September 22, 2022 are entitled to notice of and to vote at the Annual Meeting or any adjournment thereof.

Important Notice Regarding the Availability of Proxy Materials for the Annual Meeting To Be Held on November 16, 2022:

Texas Pacific Land Corporation’s Notice of Annual Meeting of Stockholders, Proxy Statement and Annual Report on Form 10-K for the fiscal year ended December 31, 2021 are available at www.proxyvote.com.

YOUR VOTE IS VERY IMPORTANT. WE HOPE YOU WILL ATTEND THIS ANNUAL MEETING. HOWEVER, WHETHER OR NOT YOU PLAN TO ATTEND THE MEETING, PLEASE PROMPTLY VOTE YOUR SHARES VIA THE INTERNET OR THE TOLL-FREE NUMBER AS DESCRIBED IN THE ENCLOSED MATERIALS. IF YOU RECEIVED A PROXY CARD BY MAIL, PLEASE SIGN, DATE AND RETURN IT IN THE ENVELOPE PROVIDED. IF YOU RECEIVED MORE THAN ONE PROXY CARD, IT IS AN INDICATION THAT YOUR SHARES ARE REGISTERED IN MORE THAN ONE ACCOUNT. PLEASE COMPLETE, DATE, SIGN AND RETURN EACH PROXY CARD YOU RECEIVE. IF YOU ATTEND THE ANNUAL MEETING AND VOTE IN PERSON, YOUR VOTE BY PROXY WILL NOT BE USED.

BY ORDER OF THE BOARD OF DIRECTORS

|

| |

Dallas, Texas

Date: October 7, 2022

|

|

|

| John R. Norris III | David E. Barry | |

| Co-Chairman | Co-Chairman |

TEXAS

PACIFIC LAND CORPORATION

1700 Pacific Avenue, Suite 2900

Dallas, TX 75201

(214) 969-5530

PROXY STATEMENT

2022 ANNUAL MEETING

OF STOCKHOLDERS

November 16, 2022

ABOUT THE ANNUAL MEETING

This proxy statement (the “Proxy Statement”) is being furnished to the stockholders of Texas Pacific Land Corporation (the “Company” or “TPL”) in connection with the solicitation of proxies by the Board of Directors of the Company (the “Board”). The proxies are for use at the 2022 Annual Meeting of Stockholders of the Company to be held on November 16, 2022, at 10:30 a.m. Central time, or at any adjournment thereof (the “Annual Meeting”) at the Renaissance Dallas Hotel, 2222 North Stemmons Freeway, Dallas, Texas 75207. In light of the ongoing COVID-19 pandemic, the Annual Meeting will be conducted in accordance with any COVID-19 protocols and requirements of the Renaissance Dallas Hotel, as well as state and local regulations, that may be in effect at the time of the Annual Meeting.

The Company consummated its corporate reorganization from a trust to a corporation (the “Corporate Reorganization”) on January 11, 2021. The trust, known as Texas Pacific Land Trust (the “Trust”) from its inception in 1888 until the Corporate Reorganization, was reorganized into a corporation formed under the laws of the State of Delaware and named Texas Pacific Land Corporation. Any references in this proxy statement to the Company, TPL, our, we, or us with respect to periods prior to January 11, 2021 refer to the Trust, and references to periods on that date and thereafter refer to Texas Pacific Land Corporation.

This Proxy Statement and the accompanying proxy card are first being mailed or made available to the stockholders on or about October 7, 2022.

THE INFORMATION PROVIDED IN THE “QUESTIONS AND ANSWERS” FORMAT BELOW IS FOR YOUR CONVENIENCE AND INCLUDES ONLY A SUMMARY OF CERTAIN INFORMATION CONTAINED IN THIS PROXY STATEMENT. YOU SHOULD READ THIS ENTIRE PROXY STATEMENT CAREFULLY.

Why am I receiving these materials?

You are receiving this Proxy Statement and the enclosed proxy card because the Board is soliciting your proxy to vote at the Annual Meeting. This Proxy Statement summarizes the information you need to vote at the Annual Meeting. You do not need to attend the Annual Meeting to vote your shares.

What are the matters to be voted on at the Annual Meeting and what are the Board’s voting recommendations?

| Board’s | More | |||||

| Proposals | ||||||

| Recommendation | Information | |||||

| Proposal 1 | Election of four directors to serve until the 2025 Annual Meeting of Stockholders | FOR each Nominee | Page 9 | |||

| Proposal 2 | Approval, by non-binding advisory vote, of the executive compensation paid to our named executive officers | FOR | Page 19 | |||

| Proposal 3 | Approval of an amendment to the Company’s Amended and Restated Certificate of Incorporation (the “Certificate of Incorporation”) providing for the declassification of the Board | FOR | Page 20 | |||

| Proposal 4 | Approval of an amendment to the Company’s Certificate of Incorporation to increase the authorized shares of common stock from 7,756,156 shares to 46,536,936 shares | FOR | Page 22 | |||

| Proposal 5 | Ratification of the appointment of Deloitte & Touche LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2022 | FOR | Page 26 | |||

| Proposal 6 | Consideration of a non-binding stockholder proposal regarding the stockholders’ right to call for a special stockholder meeting | AGAINST | Page 27 | |||

| Proposal 7 | Consideration of a non-binding stockholder proposal regarding hiring an investment banker in connection with the evaluation of a potential spinoff | AGAINST | Page 30 | |||

| Proposal 8 | Consideration of a non-binding stockholder proposal regarding the release of all remaining obligations of the stockholders’ agreement between the Company and certain stockholders | AGAINST | Page 33 | |||

| Proposal 9 | Consideration of a non-binding stockholder proposal regarding the stockholders’ right to act by written consent | AGAINST | Page 36 | |||

| Proposal 10 | Consideration of a non-binding stockholder proposal regarding director election and resignation policy. | AGAINST | Page 39 |

2

The Company knows of no other matters to be submitted to the Annual Meeting. If any other matters properly come before the Annual Meeting, it is the intention of the persons named in the accompanying form of proxy to vote the shares they represent as the Board may recommend.

How can I ask questions at the Annual Meeting?

You may ask questions relating to any matter being considered at the Annual Meeting in person at the Annual Meeting or by submitting your questions in advance by email to AnnualMeetingTPL@texaspacific.com until 11:59 p.m. Central time on November 15, 2022. We will endeavor to respond at the Annual Meeting to questions that are submitted in accordance with these guidelines. We may not be able to answer every question submitted, and if not, we may address unanswered questions with the stockholder submitting the question after the Annual Meeting.

Who may vote at the Annual Meeting?

Stockholders of record at the close of business on September 22, 2022 (the “Record Date”) are entitled to notice of and to vote at the Annual Meeting. As of the Record Date, 7,710,932 shares of the Company’s common stock, $0.01 par value (“Common Stock”), were issued and outstanding.

Each holder of Common Stock is entitled to one vote for each share of Common Stock held as of the Record Date.

What constitutes a quorum?

A majority of the voting power of all of the issued and outstanding shares of Common Stock as of the Record Date must be present, in person or by proxy, at the Annual Meeting in order to have a quorum for the transaction of business. If there is no quorum, the Annual Meeting may be adjourned to a subsequent date for the purpose of obtaining a quorum.

The inspector of elections will determine whether a quorum is present at the Annual Meeting. If you are a beneficial owner of shares of Common Stock and you do not instruct your bank, broker, trustee or other nominee how to vote your shares on any of the proposals, and your bank, broker, trustee or nominee submits a proxy with respect to your shares on a matter with respect to which discretionary voting is permitted (as discussed below), your shares will be counted as present at the Annual Meeting for purposes of determining whether a quorum exists. In addition, stockholders of record who are present at the Annual Meeting in person or by proxy will be counted as present at the Annual Meeting for purposes of determining whether a quorum exists, whether or not such holders abstain from voting on any or all of the proposals.

How many votes are required to approve each proposal?

Proposal One: Directors will be elected by the affirmative vote of a majority of the votes cast at the Annual Meeting. Abstentions and broker non-votes (if any) will have no effect on the election of directors. Our Board has adopted a “majority vote policy.” Under this policy any nominee for director in an uncontested election who does not receive a majority of the votes cast is required to tender his or her resignation following certification of the stockholder vote. The Nominating and Corporate Governance Committee will promptly consider the tendered resignation and make a recommendation to the Board whether to accept or reject the resignation.

3

Proposal Two: Approval of the non-binding advisory vote on executive compensation requires the affirmative vote of a majority of the votes cast on the matter. Abstentions and broker non-votes (if any) will have no effect on the outcome of this proposal. Because your vote on this matter is advisory, it will not be binding on the Company or the Board. However, the Compensation Committee will review the voting results and take them into consideration when making future decisions regarding executive compensation.

Proposal Three: Approval of an amendment to the Company’s Certificate of Incorporation providing for the declassification of the Board requires the affirmative vote of the majority of voting power of the outstanding shares of Common Stock entitled to vote on the matter. Abstentions and broker non-votes (if any) will have the effect of a vote “AGAINST” this proposal.

Proposal Four: Approval of an amendment to the Company’s Certificate of Incorporation increasing the amount of authorized shares of Common Stock requires the affirmative vote of the majority of voting power of the outstanding shares of Common Stock entitled to vote on the matter. Abstentions (if any) will have the effect of a vote “AGAINST” this proposal. Because brokers have discretionary authority to vote on this proposal, we do not expect any broker non-votes.

Proposal Five: Ratification of the selection of Deloitte & Touche LLP requires the affirmative vote of a majority of the votes cast on the matter. Abstentions will have no effect on the outcome of the ratification. Because brokers have discretionary authority to vote on this proposal, we do not expect any broker non-votes.

Proposal Six: Approval of the non-binding stockholder proposal regarding stockholders’ right to call for a special stockholder meeting requires the affirmative vote of a majority of the votes cast on the matter. Abstentions and broker non-votes (if any) will have no effect on the outcome of this proposal. Because your vote on this matter is advisory, it will not be binding on the Company or the Board.

Proposal Seven: Approval of the non-binding stockholder proposal regarding hiring an investment banker regarding a potential spinoff requires the affirmative vote of a majority of the votes cast on the matter. Abstentions and broker non-votes (if any) will have no effect on the outcome of this proposal. Because your vote on this matter is advisory, it will not be binding on the Company or the Board.

Proposal Eight: Approval of the non-binding stockholder proposal regarding the release of all remaining obligations of the stockholders’ agreement between the Company and certain stockholders requires the affirmative vote of a majority of the votes cast on the matter. Abstentions and broker non-votes (if any) will have no effect on the outcome of this proposal. Because your vote on this matter is advisory, it will not be binding on the Company or the Board.

Proposal Nine: Approval of the non-binding stockholder proposal regarding stockholders’ right to act by written consent requires the affirmative vote of a majority of the votes cast on the matter. Abstentions and broker non-votes (if any) will have no effect on the outcome of this proposal. Because your vote on this matter is advisory, it will not be binding on the Company or the Board.

Proposal Ten: Approval of the non-binding stockholder proposal regarding director election and resignation policy requires the affirmative vote of a majority of the votes cast on the matter. Abstentions and broker non-votes (if any) will have no effect on the outcome of this proposal. Because your vote on this matter is advisory, it will not be binding on the Company or the Board.

4

What is a broker non-vote?

A broker non-vote occurs when a broker or other nominee holding shares for a beneficial owner does not vote on a particular proposal because the broker or nominee does not have discretionary voting power for that particular item and has not received instructions from the beneficial owner. Under applicable rules that govern brokers or other nominees who are voting with respect to shares held in street name, brokers or other nominees ordinarily have the discretion to vote on “routine” matters, but not on “non-routine matters.”

The vote on Proposals One, Two, Three, Six, Seven, Eight, Nine and Ten are considered “non-routine.” Accordingly, beneficial owners who do not provide voting instructions to their brokers on these proposals will not have their shares voted with respect to such proposals. However, brokers ordinarily have authority to vote uninstructed shares for or against “routine” proposals. Proposals Four and Five constitute “routine” proposals. Accordingly, brokers that do not receive voting instructions from beneficial owners may vote on these proposals in their discretion.

How do I vote my shares without attending the Annual Meeting?

If you are a registered stockholder, you may vote by granting a proxy using any of the following methods:

| • | By Internet —If you have internet access, by submitting your proxy by following the instructions included on the enclosed proxy card. |

| • | By Telephone —By submitting your proxy by following the telephone voting instructions included on the enclosed proxy card. |

| • | By Mail —By completing, signing, and dating a proxy card (if you request paper materials from the Company) where indicated and by mailing or otherwise returning the proxy card accompanying this proxy statement in the envelope provided to you. You should sign your name exactly as it appears on the proxy card. If you are signing in a representative capacity (for example, as guardian, executor, trustee, custodian, attorney, or officer of a corporation), indicate your name and title or capacity. |

Internet and telephone voting facilities will close at 11:59 p.m. (Central Time) on November 15, 2022 for the voting of shares held by stockholders of record. Mailed proxy cards should be returned in the envelope provided to you with your proxy card and must be received by November 15, 2022.

Your vote is important, and we strongly encourage you to vote your shares by following the instructions provided on the enclosed proxy card. Please vote promptly.

If your shares are held in street name, your bank, broker, or other nominee should give you instructions for voting your shares. In these cases, you may be able to vote via the internet or by telephone, or by mail by submitting a voting instruction form by the indicated deadline.

5

Our Board of Directors has designated our Chief Executive Officer, Tyler Glover, and our Senior Vice President, General Counsel and Secretary, Micheal Dobbs, and each or any of them, as proxies to vote the shares of Common Stock solicited on its behalf.

In order for your vote to be counted, you must vote as directed in this Proxy Statement, using the proxy card provided with it or another voting method described above.

How do I vote my shares in person at the Annual Meeting?

First, you must satisfy the requirements for admission to the Annual Meeting (see below). Then, if you are a stockholder of record you may vote by ballot at the Annual Meeting. You may vote shares held in street name at the Annual Meeting only if you obtain a signed proxy from the record holder (bank, broker, or other nominee) giving you the right to vote the shares, which must be submitted with your ballot at the Annual Meeting. Even if you plan to attend the Annual Meeting, we encourage you to vote in advance so that your vote will be counted in case you later decide not to attend the Annual Meeting, as well as to speed the tabulation of votes.

How do I gain admittance to the Annual Meeting?

Only our stockholders as of the Record Date and invited guests of the Company will be permitted to attend the Annual Meeting. To gain admission, you must present a government-issued form of identification. If you are a stockholder of record, your name will be checked against our list of stockholders of record on the Record Date. If you hold shares in street name, you must present proof of your ownership of the Company’s shares as of the Record Date in order to be admitted to the Annual Meeting. Your proxy card will ask you to indicate if you intend to attend the Annual Meeting; please complete that section so that we may plan accordingly.

May I change my vote or revoke my proxy?

Any proxy given pursuant to this solicitation may be revoked by the person giving it at any time before its use by delivering to the Company’s Secretary a written notice of revocation, a duly executed proxy bearing a later date or by attending the Annual Meeting and voting in person. Any such request should be directed to the Company’s Secretary at 1700 Pacific Avenue, Suite 2900, Dallas, Texas, 75201 or (214) 969-5530. Attending the Annual Meeting in and of itself will not constitute a revocation of a proxy.

How are proxies being solicited?

Proxies may be solicited by certain of the Company’s directors, executive officers, and regular employees, without additional compensation, in person, or by telephone, e-mail or facsimile. In addition, the Company has engaged MacKenzie Partners, Inc. as paid solicitors in connection with the Annual Meeting. The anticipated cost of such service is approximately $25,000. The cost of soliciting proxies will be borne by the Company. The Company expects to reimburse brokerage firms, banks, custodians, and other persons representing beneficial owners of shares of Common Stock for their reasonable out-of-pocket expenses in forwarding solicitation material to such beneficial owners.

6

What is “householding” and will it apply to me?

Some banks, brokers and other record holders use the practice of “householding” notices, proxy statements and annual reports. “Householding” is the term used to describe the practice of delivering a single set of notices, proxy statements and annual reports to any household at which two or more stockholders reside if a company reasonably believes the stockholders are members of the same family. This procedure reduces the volume of duplicate information stockholders receive and reduces a company’s printing and mailing costs. The Company will promptly deliver an additional copy of any such document to any stockholder who writes or calls the Company. Alternatively, if you share an address with another stockholder and have received multiple copies of our notices, proxy statements and annual reports, you may contact us to request delivery of a single copy of these materials. Any such request should be directed to Investor Relations at 1700 Pacific Avenue, Suite 2900, Dallas, Texas, 75201 or (214) 969-5530.

How are proxy materials being made available to me?

Our proxy materials are available to stockholders on the Internet. This Proxy Statement and form of proxy, together with our Annual Report on Form 10-K (the “Annual Report”), are being made available to stockholders beginning approximately October 7, 2022. The Annual Report, which has been posted along with this Proxy Statement, is not a part of the proxy solicitation materials. Upon receipt of a written request, the Company will furnish to any stockholder, without charge, a copy of such Annual Report (without exhibits). Upon request and payment of $0.10 (ten cents) per page, copies of any exhibit to such Annual Report will also be provided. Any such request should be directed to the Company’s Secretary at 1700 Pacific Avenue, Suite 2900, Dallas, Texas, 75201 or (214) 969-5530. These documents are also included in our filings with the Securities and Exchange Commission (“SEC”), which you can access electronically at the SEC’s website at www.sec.gov.

How can I access the proxy materials?

You may access the proxy materials on the internet. We encourage you to review the proxy materials and to vote via the internet by following the link to the Proxy Statement and Annual Report, which are both available at www.proxyvote.com. This Proxy Statement and the Annual Report are also available on the Company’s website at www.TexasPacific.com.

Are stockholders entitled to dissenters’ rights of appraisal in connection with any proposals?

Under the Delaware General Corporation Law and the Company’s Amended and Restated Certificate of Incorporation, stockholders are not entitled to any appraisal or similar rights of dissenters with respect to any of the proposals to be acted upon at the Annual Meeting.

7

What is the deadline for receipt of stockholder proposals to be presented at the next annual meeting of stockholders?

In order for any stockholder proposal submitted pursuant to Rule 14a-8 promulgated under the Securities Exchange Act of 1934, as amended (the “Exchange Act”), to be included in the Company’s Proxy Statement to be issued in connection with the 2023 Annual Meeting of Stockholders, such stockholder proposal must be received by the Company no later than June 9, 2023. Any such stockholder proposal submitted, including any accompanying supporting statement, may not exceed 500 words, as per Rule 14a-8(d) of the Exchange Act. Any such stockholder proposals submitted outside the processes of Rule 14a-8 promulgated under the Exchange Act, which a stockholder intends to bring forth at the Company’s 2023 annual meeting of stockholders, will be untimely unless it is received between July 19, 2023 and August 18, 2023 in accordance with our bylaws. Any changes to such dates will be disclosed in our periodic reports on Form 10-Q or Form 10-K, or current reports on Form 8-K, filed with the SEC. Any such request should be directed to the Company’s Secretary at 1700 Pacific Avenue, Suite 2900, Dallas, Texas, 75201 or (214) 969-5530. In order for stockholders to give timely notice of nominations for directors, other than those nominated by the Company, for inclusion on a universal proxy card in connection with the 2023 Annual Meeting, notice must be submitted no later than September 17, 2023 and include all of the information required by Rule 14a-19 under the Exchange Act.

8

PROPOSAL ONE

ELECTION OF DIRECTORS

The Board currently consists of ten (10) directors and is divided into three (3) classes. The directors designated as “Class II” directors have terms expiring at the Annual Meeting. The directors designated as “Class I” directors have terms expiring at the 2024 annual meeting of stockholders, and the directors designated as “Class III” directors have terms expiring at the 2023 annual meeting of stockholders. At each annual meeting of stockholders, directors elected to succeed those directors whose terms then expire shall be elected for a term of office to expire at the third succeeding annual meeting of stockholders after their election, with each director holding office until his or her successor has been duly elected and qualified, subject, however, to such director’s earlier, death, resignation, disqualification or removal. Accordingly, each of the Class II directors has been nominated for election at the Annual Meeting. Each nominee has consented to being named as a nominee for election as a director and has agreed to serve if elected; however, if a nominee should withdraw his or her name from consideration for any reason or otherwise become unable to serve before the Annual Meeting, the Board reserves the right to substitute another person as nominee, and the persons named on your proxy card as proxies will vote for any substitute nominated by the Board.

Stockholders’ Agreement

The stockholders’ agreement (the “Stockholders’ Agreement”) was entered into on June 11, 2020, by and among the Trust (and later assigned to the Company), Horizon Kinetics LLC and Horizon Kinetics Asset Management LLC (together with Horizon Kinetics LLC and its affiliates, “Horizon”), SoftVest Advisors, LLC (“SoftVest Advisors”) and SoftVest, L.P. (together with SoftVest Advisors and its affiliates, “SoftVest,” and together with Horizon, the “Investor Group”), and Mission Advisors, LP (“Mission” and together with the Investor Group, collectively, the “stockholder parties”). Pursuant to the Stockholders’ Agreement, the Company agreed that (a) the Board shall be divided into three classes of directors, with directors in each class serving staggered, three-year terms and (b) (i) Dana F. McGinnis, the director designated by Mission (the “Mission Designee”), would be appointed to Class I of the Board, (ii) Eric L. Oliver, the director designated by SoftVest (the “SoftVest Designee”), would be appointed to Class II of the Board, and (iii) Murray Stahl, the director designated by Horizon (the “Horizon Designee” and together with the SoftVest Designee and the Mission Designee, the “Stockholder Designees”), would be appointed to Class III of the Board. Such appointments were made in connection with the Corporate Reorganization. Mr. McGinnis resigned from the Board in March 2022.

9

As a condition to appointment to the Board, the Horizon Designee has provided an executed conditional resignation letter pursuant to which he has irrevocably offered to resign from his position as a director of the Board and from any and all committees of the Board, effective upon the earliest to occur of (a) Horizon ceasing to beneficially own 10% of the issued and outstanding shares of Common Stock (the “Minimum Ownership Event”) and (b) the completion of the Annual Meeting. The SoftVest Designee, as a condition to appointment to the Board, has provided to the Board an executed conditional resignation letter pursuant to which he has irrevocably offered to resign from his position as a director of the Board and from any and all committees of the Board effective upon the earliest to occur of (a) the Minimum Ownership Event, (b) the Horizon Designee ceasing to serve on the Board and (c) the completion of the Annual Meeting. The Board has not determined if or when it will accept the resignations under either or both of the conditional resignation letters.

As a further condition to the appointment of the Stockholder Designees to the Board, the Trust, the trustees of the Trust, consisting of John R. Norris III and David E. Barry (the “Trustees”), and the stockholder parties executed a mutual general release agreement. Pursuant to the mutual general release agreement, each party thereto released each other party thereto from all claims and liabilities arising prior to the execution of the Stockholders’ Agreement and in connection with the investor litigation among the Investor Group and the Trust (which litigation was settled pursuant to a settlement agreement dated as of June 30, 2019 (the “Settlement Agreement”)). The Trust and the Trustees entered into the mutual general release agreement prior to the Corporate Reorganization. Pursuant to the Stockholders’ Agreement, in connection with the Corporate Reorganization, the Trust conveyed, and the Company assumed, all of the Trust’s rights and obligations under the Stockholders’ Agreement.

Pursuant to the Stockholders’ Agreement, the stockholder parties have agreed to vote all of the shares of Common Stock they beneficially own at each annual or special meeting of stockholders of the Company in accordance with the Board’s recommendations, subject to certain exceptions. The termination date of the Stockholders’ Agreement is immediately following the completion of the 2022 Annual Meeting, provided, however, that the respective obligations of the investor group shall survive until such time as neither Investor Group designee is serving on the Board.

Board of Directors

The following table sets forth information with respect to our directors and is followed by biographies of each such individual.

| Name | Age | Title/Class | ||

| David E. Barry | 77 | Director, Class III; Co-Chair | ||

| Rhys J. Best | 75 | Director, Class II | ||

| General Donald G. Cook, USAF (Ret.) | 76 | Director, Class II | ||

| Barbara J. Duganier | 64 | Director, Class I | ||

| Donna E. Epps | 58 | Director, Class II | ||

| Karl F. Kurz | 61 | Director, Class I | ||

| John R. Norris III | 69 | Director, Class III; Co-Chair | ||

| Eric L. Oliver | 63 | Director, Class II | ||

| Murray Stahl | 68 | Director, Class III | ||

| Tyler Glover | 37 | Director, Class I; President and Chief Executive Officer |

10

CLASS II DIRECTORS

Terms Expiring at the Annual Meeting

Rhys J. Best

Mr. Best has been a member of the Board since April 15, 2022. Mr. Best currently serves on the board of Arcosa Inc. (NYSE: ACA) (since 2018), where he serves as the non-executive Chairman of the Board. Mr. Best previously served on the board of Cabot Oil and Gas Corp. (from 2008 to 2021), his term ending after the company merged with Cimarex Energy in 2021 to form Coterra Energy (NYSE: CTRA). Mr. Best also previously served on the boards of Commercial Metals Company (NYSE: CMC) (from 2010 to 2022), Crosstex Energy, LP, an integrated, multi-commodity midstream enterprise (NASDAQ: XTEX) (from 2004 to 2014, including serving as Chairman of the Board from 2009 to 2014), MRC Global, Inc., a pipe, valve and fitting distribution business (NYSE: MRC) (from 2008 to 2022, including serving as Chairman of the Board from 2016 to 2022), Trinity Industries, Inc. (NYSE: TRN) (from 2005 to 2018), and Austin Industries, an employee-owned construction company (from 2007 to 2018, including serving as Chairman of the Board from 2013 to 2018). Mr. Best is the former Chairman and Chief Executive Officer of Lone Star Technologies, Inc., an energy services and supply company, a role he retired from in 2007 after the successful merger with United States Steel Company (NYSE: X).

Mr. Best serves on the Nominating and Corporate Governance Committee of the Board.

Mr. Best’s qualifications to serve as a director include his extensive business experience, including in the oil and gas industry, and governance experience.

11

Donald G. Cook

Gen. Cook has been a member of the Board since January 11, 2021. Gen. Cook currently serves on the board of Cybernance, Inc. (since 2016). Gen. Cook previously served on the boards of Crane Co. (from 2005 to 2022), USAA Federal Savings Bank (from 2007 to 2018), U.S. Security Associates Inc., a Goldman Sachs portfolio company (from 2011 to 2018), and Beechcraft LLC, formerly known as Hawker Beechcraft Inc. (from 2007 to 2014). Gen. Cook served on the board of Burlington Northern Santa Fe Railroad for almost five years until it was sold to Berkshire Hathaway in 2010 in a transaction valued at $44 billion. He also consults for Lockheed Martin Corporation. In addition to his extensive corporate governance experience, Gen. Cook has been the Chairman of the San Antonio advisory board of the NACD Texas TriCities Chapter, a group recognized as the authority on leading boardroom practices. Gen. Cook had numerous additional command and high-level staff assignments during his 36-year career with the Air Force and retired as a four-star General. He commanded a flying training wing and two space wings, the 20th Air Force (the nation’s nuclear Intercontinental Ballistic Missile force) and was interim Commander of Air Combat Command during the September 11 attacks. Gen. Cook served as the Chief of the Senate Liaison Office and on the staff of the House Armed Services Committee in the U.S. House of Representatives. Prior to his retirement from the Air Force in August 2005, Gen. Cook’s culminating assignment was Commander, Air Education and Training Command at Randolph Air Force Base in Texas, where he was responsible for executing the $8 billion annual budget to recruit, train and educate Air Force personnel, safely implementing the 500,000-hour annual flying hour program and providing for the leadership, welfare, and oversight of 90,000 military and civilian personnel in the command. He was twice awarded the Distinguished Service Medal for exceptional leadership.

Gen. Cook serves on and is the chairperson of the Nominating and Corporate Governance Committee of the Board.

General Cook also serves on the Compensation Committee of the Board. |  |

Gen. Cook’s qualifications to serve as a director include his extensive experience with corporate governance and executive compensation, as well as managerial experience resulting from his tenure of command in the U.S. Air Force.

12

Donna E. Epps

Ms. Epps has been a member of the Board since January 11, 2021. Ms. Epps currently serves on the board of Saia, Inc. (Nasdaq: SAIA) (since 2019), where she serves on the audit committee and the nominating and governance committee, and on the board of Texas Roadhouse, Inc. (Nasdaq: TXRH), where she serves on the audit committee, the nominating and governance committee and the compensation committee. Ms. Epps was with Deloitte LLP, a multinational professional services network, for over 30 years. Ms. Epps served as an attest Partner of Deloitte LLP from 1998 through 2003 and as a Risk and Financial Advisory Partner of Deloitte LLP from 2004 until her retirement in 2017. During her time at Deloitte LLP, Ms. Epps helped companies develop and implement proactive enterprise risk and compliance programs, focusing on value protection and creation, and provided attest services and financial advisory services in governance, risk and compliance matters to private and public companies across multiple industries. Ms. Epps is currently a licensed certified public accountant and a member of the North Texas Association of Corporate Directors Board. Ms. Epps is Chair of the Girl Scouts of Northeast Texas since April 2021 and Treasurer of Readers2Leaders in Dallas, Texas since 2019.

Ms. Epps serves on and is the chairperson of the Audit Committee of the Board. Ms. Epps also serves on the Nominating and Corporate Governance Committee of the Board.

Ms. Epps’s significant audit, governance, risk, and compliance experience as a provider of attest and consulting services to private and public companies across multiple industries makes her well-qualified to serve on the Board. |  |

13

Eric L. Oliver

Mr. Oliver has been a member of the Board since January 11, 2021. Mr. Oliver currently serves as the President of SoftVest Advisors, a registered investment adviser that acts as an investment manager for private fund clients. Mr. Oliver additionally serves as the President of HeartsBluff Music Partners, LLC and Carrizo Springs Music Partners, LLC, both of which are registered investment advisers pursuant to an umbrella registration filed by SoftVest Advisors, LLC. Previously, Mr. Oliver was President of Midland Map Company, LLC, a Permian Basin oil and gas lease and ownership map producer from 1997 until its sale in January of 2019 to Drilling- Info, and was Principal of Geologic Research Centers LLC, a log library providing geological data to the oil and gas industry with a library in Abilene, Texas, sold in 2019. Additionally, Mr. Oliver served on the board of Texas Mutual Insurance Company from 2009 until he retired in July 2021. He has also served as a director on the board of AMEN Properties, Inc. (OTC: AMEN) since July 2001 and was appointed Chairman of the Board in September 2002. AMEN Properties directly or indirectly owns certain oil and gas royalty and working interest properties. Furthermore, Mr. Oliver serves on the board of Abilene Christian Investment Management Company, Abilene Christian University’s endowment management company, and is a former member of the Abilene Community Foundation’s investment committee. Mr. Oliver received a B.A. in Chemistry from Abilene Christian University in 1981. Mr. Oliver is the Softvest Designee pursuant to the Stockholders’ Agreement.

Mr. Oliver serves on the Audit Committee of the Board.

Mr. Oliver’s qualifications to serve as a director include his experience as an oil and gas investor, with over 22 years of experience buying and selling mineral and royalty properties, and over 35 years of experience managing investments with an emphasis in the energy market. |  |

14

CLASS I DIRECTORS

Terms Continue Until 2024

Barbara J. Duganier

Ms. Duganier has been a member of the Board since January 11, 2021. Ms. Duganier currently serves on the board of MRC Global Inc. (NYSE: MRC) (since 2015), an industrial distributor of pipe, valves and other related products and services to the energy industry, where she chairs the audit committee and serves on the ESG and enterprise risk committee. Ms. Duganier also serves on the boards of two private companies: McDermott International, Ltd. (since 2020), a fully-integrated provider of engineering and construction solutions to the energy industry, where she chairs the audit committee and serves on the risk committee; and Pattern Energy Group LP (since 2020), a private renewable energy company focused on wind, solar, transmission and storage where she chairs the audit committee. Ms. Duganier previously served on the boards of the general partner of Buckeye Partners, L.P. (NYSE: BPL), a midstream oil and gas master limited partnership, where she chaired the audit committee and served on the compensation committee until the company’s sale in November 2019; of Noble Energy (Nasdaq: NBL), an exploration and production company, where she served as a member of the audit and nominating and governance committees until the company’s sale in October 2020; and West Monroe Partners, a management and technology consulting firm, where she was the lead independent director and nominating and governance committee chair until the sale of the company in November 2021. Ms. Duganier is also a former director and member of the enterprise and risk oversight and compensation committees of HCC Insurance Holdings, a property and casualty insurance underwriter, which was sold in 2015. From 2004 to 2013, Ms. Duganier was a Managing Director at Accenture, a multinational professional services company that provides services in strategy, consulting, digital technology, and operations. She held various leadership and management positions in Accenture’s outsourcing business, including Global Chief Strategy Officer and Global Growth and Offering Development Lead. A year prior to joining Accenture, she served as an independent consultant to Duke Energy North America. From 1979 to 2002, Ms. Duganier, who is a licensed certified public accountant, worked at Arthur Andersen LLP, where she served as an auditor and financial consultant, as well as in various leadership and management roles, including Global Chief Financial Officer of Andersen Worldwide. Ms. Duganier also serves on the board of John Carroll University and as former Chairman of the Board of the National Association of Corporate Directors (NACD) Texas TriCities chapter.

Ms. Duganier serves on and is the chairperson of the Compensation Committee of the Board and serves on the Audit Committee of the Board.

Ms. Duganier’s extensive executive experience overseeing large organizations, her diverse board experience and her credentials as a certified public accountant make her well-qualified to serve on the Board. |  |

15

Tyler Glover

Mr. Glover has been a member of the Board since January 11, 2021. Mr. Glover serves as the Company’s President and Chief Executive Officer. Mr. Glover served as Chief Executive Officer, Co-General Agent and Secretary of the Trust, in which capacity he acted since November 2016, and also currently serves as President and Chief Executive Officer of Texas Pacific Water Resources LLC, a wholly owned subsidiary of the Company (“TPWR”), in which capacity he has acted since its formation in June 2017. Mr. Glover previously served as Assistant General Agent of the Trust from December 2014 to November 2016 and has over 10 years of energy services and land management experience.

Mr. Glover’s qualifications to serve as a director include his extensive industry expertise and experience as an officer at the Company, including at the Trust. |  |

| Karl F. Kurz

Mr. Kurz has been a member of the Board since April 15, 2022. Mr. Kurz is currently a non-executive Chairman of the board at American Water Works Co., Inc. (NYSE: AWK) and a member of the board at Devon Energy Corporation (NYSE: DVN) where he serves on the Compensation Committee, Governance, Environmental & Public Policy Committee and Reserves Committee. Mr. Kurz previously served on the board of Global Geophysical Services Inc. (NYSE: GGS), SemGroup Corporation (NYSE: SEMG), Western Gas Partners LP (NYSE:WES), WPX Energy Inc. (NYSE: WPX), Chaparral Energy Inc. (private) and Siluria Technologies Inc. (private). Mr. Kurz spent nine years at Anadarko Petroleum Corporation, where he held roles as Chief Operating Officer and Senior Vice President of Northern America Operations, Midstream and Marketing. Mr. Kurz also has extensive private equity experience that includes serving as a senior investment executive at Ares Capital and CCMP Capital Advisors, where he focused on investments in the oil and gas upstream and midstream sectors.

Mr. Kurz serves on the Compensation Committee of the Board.

Mr. Kurz’s qualifications to serve as a director include his extensive business experience, including in the oil and gas industry in Texas, and governance experience. |

16

CLASS III DIRECTORS

TERMS CONTINUE UNTIL 2023

|

David E. Barry

Mr. Barry serves as a Co-Chair of the Board. Mr. Barry served as a Trustee of the Trust from 2017 to January 11, 2021 and has been a member of the Board since January 11, 2021. Mr. Barry has served as president of Tarka Resources, Inc., which is engaged in oil and gas exploration in Texas, Oklahoma and Louisiana, since 2012. He also served as President of Tarka, Inc. from 2012 through 2014, until such company was merged with Tarka Resources, Inc. in 2016. Mr. Barry practiced real estate, employee benefits and compensation law at the law firm of Kelley Drye & Warren LLP (“Kelley Drye”) from 1969, becoming a partner in 1978. Mr. Barry represented the Trust for more than 30 years as a partner at Kelley Drye. Mr. Barry retired from Kelley Drye in 2014. Beginning in 2007 and then full-time starting in 2012, Mr. Barry has worked as President of Sidra Real Estate, Inc., an entity with commercial real estate holdings throughout the United States.

Mr. Barry’s qualifications to serve as a director include his legal expertise and knowledge gained over a 51-year career at Kelley Drye, including representing the Trust for more than 30 years prior to his election as a Trustee, as well as his experience in commercial real estate, including commercial real estate in Texas. |

|

| John R. Norris III

Mr. Norris serves as a Co-Chair of the Board. Mr. Norris served as a Trustee of the Trust from 2000 to January 11, 2021 and has been a member of the Board since January 11, 2021. Mr. Norris is a member with the law firm Norris & Weber, PLLC (“Norris & Weber”) in Dallas, Texas. Mr. Norris began working with a predecessor firm of Norris & Weber in 1979 and has stayed with the firm throughout the past 40 years. He has been continuously certified as a legal specialist in estate planning and probate law by the Texas Board of Legal Specialization since 1989. In 1995, he was elected as a Fellow of the American College of Trusts and Estate Counsel, a professional association of lawyers throughout the United States who have been recognized as outstanding practitioners in the laws of wills, trusts, estate planning and administration and related tax planning. Mr. Norris is a member of the State Bar of Texas and the Dallas Bar Association, where he served as Chairman of the Probate, Trust & Estate section in 1995. Mr. Norris was a member of the District 6A Grievance Committee of the State Bar of Texas between 1995 and 2001, serving as its Chairperson between 1998 and 2000.

Mr. Norris’ qualifications to serve as a director include his extensive background as a practicing attorney in Dallas, Texas. In addition to his 20 years of experience as a Trustee, Mr. Norris advised and represented the Trust on legal matters for more than 17 years prior to his election as a Trustee.

|

17

Murray Stahl

Mr. Stahl has been a member of the Board since January 11, 2021. Mr. Stahl is the Chief Executive Officer, Chairman of the Board and co-founder of Horizon Kinetics LLC and serves as Chief Investment Officer of Horizon Kinetics Asset Management LLC, a wholly owned subsidiary of Horizon Kinetics LLC. He has over 30 years of investing experience and is responsible for overseeing Horizon Kinetics’ proprietary research and chairs the firm’s investment committee, which is responsible for portfolio management decisions across the entire firm. He is also the Co-Portfolio Manager for a number of registered investment companies, private funds, and institutional separate accounts. Mr. Stahl is the Chairman and Chief Executive Officer of FRMO Corp. (OTC: FRMO) and has been a director since 2001. He is also a member of the board of RENN Fund, Inc. (NYSE: RCG) (since 2017), the Bermuda Stock Exchange, MSRH, LLC, and the Minneapolis Grain Exchange. He was a member of the board of Winland Electronics, Inc. (from 2015 to 2020) and IL&FS Securities Services Limited (from 2008 to 2020). Prior to co-founding Horizon Kinetics, Mr. Stahl spent 16 years at Bankers Trust Company (from 1978 to 1994) as a senior portfolio manager and research analyst. As a senior fund manager, he was responsible for investing the Utility Mutual Fund, along with three of the bank’s Common Trust Funds: The Special Opportunity Fund, The Utility Fund and The Tangible Assets Fund. He was also a member of the Equity Strategy Group and the Investment Strategy Group, which established asset allocation guidelines for the Private Bank. Mr. Stahl is the Horizon Designee pursuant to the Stockholders’ Agreement.

Mr. Stahl serves on the Nominating and Corporate Governance Committee of the Board.

Mr. Stahl’s qualifications to serve as a director include his over 30 years of investment experience, including in the energy and minerals space. |  |

THE BOARD OF DIRECTORS RECOMMENDS A VOTE “FOR” THE ELECTION OF RHYS J. BEST, DONALD G. COOK, DONNA E. EPPS AND ERIC L. OLIVER AS CLASS II DIRECTORS.

18

PROPOSAL TWO

NON-BINDING ADVISORY VOTE ON EXECUTIVE COMPENSATION

SEC rules adopted pursuant to the Dodd-Frank Wall Street Reform and Consumer Protection Act, enacted in July 2010, enable our stockholders to vote to approve, on a non-binding, advisory basis, the compensation of our named executive officers as disclosed in this proxy statement.

We believe that our executive compensation programs must be closely linked to our stockholders’ interests, and we welcome our stockholders’ input in this area. Our compensation programs are designed to attract, motivate, and retain the individuals we need to drive business success. Beginning in December 2021, we have been able to incorporate equity compensation into our compensation packages, which previously had consisted solely of cash, paid in the form of base salary and bonus. Please read the Compensation Discussion and Analysis, the Summary Compensation Table and the other related tables and accompanying narrative for a detailed description of the fiscal year 2021 compensation of our named executive officers. We believe that the 2021 compensation of each of our named executive officers was reasonable and appropriate and was aligned with the Company’s 2021 results.

The vote on this resolution is not intended to address any specific element of compensation; rather, the vote relates to the overall compensation of our named executive officers. This vote is advisory only and is not binding on the Company or the Board. Although the vote is non-binding, our Board values the opinions of our stockholders and the Board, and the Compensation Committee will consider the outcome of the vote when making future compensation decisions for our named executive officers.

Approval of this proposal requires the affirmative vote of a majority of the votes cast on the matter. Abstentions and broker non-votes will have no effect on the outcome of this proposal.

Accordingly, we ask our stockholders to vote in favor of the following resolution:

“RESOLVED, that the Company’s stockholders approve, on a non-binding, advisory basis, the compensation of the named executive officers, as disclosed in the Company’s Proxy Statement for the 2022 Annual Meeting of Stockholders pursuant to the compensation disclosure rules of the Securities and Exchange Commission.”

THE BOARD OF DIRECTORS RECOMMENDS A VOTE “FOR” APPROVAL, ON A NON-BINDING ADVISORY BASIS, OF THE COMPENSATION OF OUR NAMED EXECUTIVE OFFICERS.

19

PROPOSAL THREE

APPROVAL OF AN AMENDMENT TO THE CERTIFICATE OF INCORPORATION PROVIDING FOR THE DECLASSIFICATION OF THE BOARD

The Company’s Certificate of Incorporation divides the Board members into three (3) classes. One class is elected at each annual meeting of stockholders, to hold office for a term beginning on the date of the election and expiring at the third annual meeting of stockholders thereafter.

Upon the recommendation of our Nominating and Corporate Governance Committee, the Board has determined that it is advisable and in the best interests of the stockholders to declassify the Board to allow for a vote on the election of the entire Board each year, rather than on a staggered basis. The draft Second Amended and Restated Certificate of Incorporation, which has been approved, adopted and determined advisable and in the best interests of the Company by the Board, subject to stockholder approval, is set forth in Appendix A to this Proxy Statement (the “Declassification Amendment”), and the description of the Declassification Amendment set forth below is qualified in its entirety by reference to the text of the Declassification Amendment. We believe this amendment reflects our commitment to good corporate governance and better aligns our governance processes with what is considered to be governance best practices by the investor community.

If the Declassification Amendment becomes effective, commencing at the 2023 annual meeting of stockholders, all directors standing for election will become subject to election on an annual basis for a one-year term. The division of directors into classes shall terminate at the 2025 annual meeting of stockholders, with the expiration of the term of the directors elected at the Annual Meeting. Vacancies which may occur during the year may be filled by the Board and each director so appointed shall serve for a term expiring at the next election of the class for which such director shall have been chosen or, following the termination of the division of directors into classes, for a term expiring at the next annual meeting of stockholders. If the stockholders do not approve this proposal, then the Board will remain classified, with each class of directors serving a term of three years. Notwithstanding the foregoing, in all cases, each director will hold office until his or her successor is duly elected, or until his or her earlier resignation or removal.

The following table illustrates the timing of the transition from three-year terms to one-year terms if this proposal is approved by stockholders and the Declassification Amendment becomes effective:

| 2021 | 2022 | 2023 | 2024 | 2025 | 2026 | |

| Current Classified Board Structure | Class I

(3-Year Term) |

Class I

(3-Year Term) |

||||

| Class II

(3-Year Term) |

Class II

(3-Year Term) |

|||||

| Class III

(3-Year Term) |

Class III

(3-Year Term) | |||||

|

2025 Phased Declassification beginning with 2023 Annual Meeting |

Class I

(3-Year Term) |

Class I

(1-Year Term) |

All on 1-Year Term | All on 1-Year Term | ||

| Class II

(3-Year Term) |

||||||

| Class III

(1-Year Term) |

Class III

(1-Year Term) |

20

Currently, our Certificate of Incorporation allows for removal of directors by our stockholders only for cause. Under Delaware corporate law, directors of companies that have a classified board structure may be removed only for cause unless the Certificate of Incorporation provides otherwise, while directors of companies that do not have a classified board may be removed with or without cause. Accordingly, the Declassification Amendment also provides that any director elected for a three-year term, and any director who will stand for re-election at the 2023 annual meeting of stockholders, shall be removable only for cause during such term, and that any director elected for a one-year term shall be removable either with or without cause.

The Board recognizes that a classified structure may offer several advantages, such as promoting board continuity and stability, encouraging directors to take a long-term perspective, and providing protection against certain abusive takeover tactics. The Board also recognizes that a classified structure may reduce directors’ accountability to stockholders because such a structure does not enable stockholders to express a view on each director’s performance by means of an annual vote. Moreover, many institutional investors believe that the election of directors is the primary means for stockholders to influence corporate governance policies and to hold management accountable for implementing those policies.

At the time of our Corporate Reorganization, the Trustees of the Trust believed that a classified board would best protect and provide stability to the Company during the transition from a trust to a Delaware corporation, which transition was effected January 11, 2021. In determining whether to support the declassification of the Board, the Board considered the arguments in favor of and against continuation of the classified board structure and determined that it was advisable and would be in the best interests of the Company and the stockholders to declassify the Board.

If our stockholders approve the Declassification Amendment, the Declassification Amendment will become effective upon filing a Certificate of Amendment with the Delaware Secretary of State. The Board intends to cause such filing promptly following stockholder approval, but the Board nevertheless would retain the discretion under Delaware law, until such time, to not implement the Declassification Amendment. In such case, the staggered structure of the Board would accordingly remain.

THE BOARD RECOMMENDS A VOTE “FOR” APPROVAL OF AN AMENDMENT TO THE CERTIFICATE OF INCORPORATION PROVIDING FOR THE DECLASSIFICATION OF THE BOARD.

21

PROPOSAL FOUR

APPROVAL OF AN AMENDMENT TO THE CERTIFICATE OF INCORPORATION INCREASING THE NUMBER OF SHARES OF AUTHORIZED COMMON STOCK

The Board recommends that stockholders consider and vote in favor of the adoption of an amendment (the “Authorized Shares Amendment”) to Article IV of the Amended and Restated Certificate of Incorporation of the Company (the “Certificate”) that would increase the authorized number of shares of common stock of the Company, par value $0.01 per share, (the “Common Stock”) from 7,756,156 shares (as presently authorized) to 46,536,936 shares. The Board has adopted the Authorized Shares Amendment, subject to stockholder approval, and declared it to be advisable and in the best interests of the Company.

Section 4.1(A) of Article IV of the Certificate, marked to show the Authorized Shares Amendment, is as follows:

(A) The total number of shares

of stock that the Corporation shall have authority to issue is 8,756,156 47,536,936 shares of stock, classified as:

| (1) | 1,000,000 shares of preferred stock, par value $0.01 per share (“Preferred Stock”); and |

| (2) |

Purposes of Increasing the Number of Shares of Authorized Common Stock; Potential Stock Split in the Form of a Stock Dividend

In connection with the Corporate Reorganization, the number of authorized shares of Common Stock was fixed in the Certificate to be equal to the number of shares of the Trust (the “sub-share certificates”) that were outstanding as of immediately prior to the Corporate Reorganization. This was done in part to allow the newly-created Board to determine, in the future, whether to approve the authorization of additional shares of Common Stock through an amendment to the Certificate and to propose the same for approval by stockholders of the Company.

The Certificate currently authorizes the issuance of a total of 8,756,156 shares of stock. Of such shares, 7,756,156 are classified as Common Stock and 1,000,000 are classified as preferred stock. Pursuant to the Corporate Reorganization, on January 11, 2021, the Company issued and distributed 7,756,156 shares of Common Stock to all of the holders of the sub-share certificates as of immediately prior to the Corporate Reorganization.

22

As of September 22, 2022, there were 7,710,932 shares of Common Stock issued and outstanding and no shares of preferred stock issued or outstanding. In addition to this number of shares of Common Stock outstanding, as of September 22, 2022, the Company had 45,224 shares of Common Stock held in treasury, of which 10,400 shares of Common Stock were reserved for issuance for awards granted pursuant to the 2021 Incentive Plan.

Unlike almost every company in the S&P 500 or S&P Midcap 400, the Company does not have any authorized but unissued shares of Common Stock available for future issuances. The only shares of Common Stock that are available to the Company for future issuances are its limited treasury shares. The Company may use available treasury shares as it deems fit for new issuances of Common Stock, such as under the 2021 Incentive Plan or the 2021 Non-Employee Director Stock and Deferred Compensation Plan (the “2021 Directors Plan” and together with the 2021 Incentive Plan, the “Incentive Plans”), or as consideration for acquisitions (as further described below). The primary method by which the Company can acquire more treasury shares is by reacquiring outstanding shares of Common Stock through stock repurchases.

If stockholders approve the Authorized Shares Amendment, it would permit the Board to effect a potential 3-for-1 split of the Company’s Common Stock in the form of a stock dividend of 2 shares per outstanding share totaling 15,421,864 based on the number of shares outstanding on September 22, 2022 (the “Stock Split”). Currently, the number of shares of Common Stock authorized, but not outstanding and not reserved for issuance for any specific purpose, is insufficient to effectuate the Stock Split. The increase in authorized shares will provide the Company with the ability to effect the Stock Split to lower the price per share of Common Stock to attract a broader investor base and increase stock liquidity. The Board has approved the Stock Split, subject to the Authorized Shares Amendment and there not being any material changes in the Company’s financial condition or results of operation or the market price for the Common Stock that would cause the Board to change its view on the desirability of effecting the Stock Split.

The Company could additionally use its ability to issue additional Common Stock for other purposes in the future, including: the sale of securities to raise capital; payment of consideration for acquisitions; payment of stock dividends; grants made to employees under new or expanded existing compensation plans or arrangements; and other corporate purposes. An increase in the number of authorized shares of Common Stock would also provide the Company with flexibility with respect to future transactions, including acquisitions of additional assets where the Company would have the option to use its Common Stock (or securities convertible into or exercisable or exchangeable for Common Stock) as consideration (rather than cash), financing future growth, financing transactions and other general corporate purposes. Any of such transactions, facilitated by the issuance of additional shares of Common Stock, could have the potential to benefit the Company and stockholders by, among other things, growing the Company’s business or assets, increasing stockholder value, or increasing the marketability and liquidity of the Common Stock.

23

Other than with respect to the Stock Split and under the Incentive Plans, the Company does not have any present intention to issue Common Stock in the immediate future. The submission of this Proposal Four is not part of any other existing plan of the Board to engage in any transaction that would require the proposed increase. However, the Company desires to have the flexibility to use Common Stock as consideration for the acquisition of additional assets. Authorized but unissued shares of Common Stock may be used by the Company from time to time as appropriate and opportune situations arise. The ability to issue additional shares would enable the Company to act quickly as opportunities arise and to avoid the time-consuming and costly need to hold a special meeting of stockholders in every case to seek stockholder approval for the issuance of additional shares of Common Stock. The Board believes that, in the future, occasions may arise where the time required to obtain stockholder approval might adversely delay or prohibit the Company’s ability to enter into a desirable transaction or deny it the flexibility to facilitate the effective use of its securities. Therefore, failure to approve this Proposal Four, in addition to prohibiting the Stock Split, could, in effect, prevent the Company from pursing strategic acquisitions.

Effects of the Authorized Shares Amendment

For the reasons discussed above, the Board believes that it is in the best interests of the Company to increase the number of authorized shares of Common Stock.

If this Proposal Four is approved by stockholders, the Company’s current Certificate will be amended to increase the number of shares of authorized stock of the Company to 47,536,936 shares of stock, of which 46,536,936 shares would be classified as Common Stock. The additional, newly-authorized shares of Common Stock would be part of the existing class of Common Stock and, if and when issued, would have rights identical to the currently issued and outstanding Common Stock. The Authorized Shares Amendment would not affect the number of shares of preferred stock authorized.

The Authorized Shares Amendment would not change any of the rights, restrictions, terms or provisions relating to the Common Stock or any preferred stock that may be issued in the future. Under the Delaware General Corporation Law (the “DGCL”), stockholders of the Company will not be entitled to appraisal rights with respect to the Authorized Shares Amendment and will not have any preemptive rights with respect to the additional shares being authorized. No further approval by stockholders would be necessary prior to the issuance of any additional shares of Common Stock, except as may be required by law or applicable NYSE rules. In certain circumstances, generally relating to the number of shares to be issued and the identity of the recipient, the rules of the NYSE require stockholder authorization in connection with the issuance of such additional shares (i.e., stockholder approval is generally required for stock issuances if the number of shares of common stock to be issued is equal to or in excess of 20% of the number of shares of common stock outstanding, otherwise than through a cash public offering). Subject to Delaware law and the rules of the NYSE, the Board has the sole discretion to issue additional shares of Common Stock for such consideration as may be determined by the Board.

The issuance of any additional shares of Common Stock may have the effect of diluting the percentage of stock ownership of present stockholders of the Company. Furthermore, although the Board has not recommended the Authorized Shares Amendment in order to discourage tender offers or takeover attempts of the Company, the availability of more authorized shares of Common Stock for issuance may have the effect of discouraging a merger, tender offer, proxy contest or other attempt to obtain control of the Company.

24

If the Authorized Shares Amendment is adopted, it will become effective upon filing a Certificate of Amendment with the Delaware Secretary of State. The Board intends to cause such filing promptly following stockholder approval, but the Board nevertheless would retain the discretion under Delaware law, until such time, to not implement the Authorized Shares Amendment. In such case, the number of authorized shares would accordingly remain at its current level.

Effect of the Stock Split

If stockholders adopt the Authorized Shares Amendment and the Company subsequently undertakes and consummates the Stock Split, the amount of the Company’s Common Stock account as reflected in the Company’s consolidated financial statements will be increased to reflect the additional shares issues at a par value of $0.01 per share and the amount of the additional paid-in capital account will be reduced by the same amount, with no overall net effect on total stockholders’ equity. Further, pursuant to the anti-dilution adjustment provisions of the Incentive Plans, proportionate adjustments would be made to the number of shares of Common Stock that remain available for issuance pursuant to such plans, as well as the outstanding awards under such plans.

THE BOARD RECOMMENDS A VOTE “FOR” APPROVAL OF AN AMENDMENT TO THE CERTIFICATE OF INCORPORATION INCREASING THE NUMBER OF SHARES OF AUTHORIZED COMMON STOCK.

25

PROPOSAL FIVE

RATIFICATION OF THE APPOINTMENT OF OUR INDEPENDENT REGISTERED PUBLIC ACCOUNTING FIRM

The Board has selected Deloitte & Touche LLP as our independent registered public accounting firm for the fiscal year ending December 31, 2022, subject to ratification by our stockholders at the Annual Meeting. Deloitte & Touche LLP has been our independent registered public accounting firm since April 2021. A representative of Deloitte & Touche LLP is expected to be present at the Annual Meeting, will have the opportunity to make a statement if he or she desires to do so, and is expected to be available to respond to appropriate questions.

Neither the Company nor anyone on its behalf has consulted with Deloitte & Touche LLP with respect to (1) the application of accounting principles to a specified transaction, either completed or proposed, or the type of audit opinion that might be rendered on the Company’s financial statements, and neither a written report was provided to the Company nor oral advice was provided that Deloitte & Touche LLP concluded was an important factor considered by the Company in reaching a decision as to the accounting, auditing, or financial reporting issue or (2) any matter that was either the subject of a disagreement (as defined in Item 304(a)(1)(iv) of Regulation S-K and the related instructions) or a reportable event (as described in Item 304(a)(1)(v) of Regulation S-K).

More information about our independent registered public accounting firm is available under the heading “Independent Registered Public Accounting Firm” on page 82 below.

THE BOARD OF DIRECTORS RECOMMENDS THAT YOU VOTE “FOR” THE RATIFICATION OF THE APPOINTMENT OF DELOITTE & TOUCHE LLP AS OUR INDEPENDENT AUDITOR FOR THE FISCAL YEAR ENDING DECEMBER 31, 2022.

26

PROPOSAL SIX

STOCKHOLDER PROPOSAL REGARDING A STOCKHOLDERS’ RIGHT TO CALL FOR A SPECIAL STOCKHOLDER MEETING

The following proposal was submitted by Lawrence J. Goldstein, a stockholder of the Company. Mr. Goldstein has informed the Company that he is the beneficial owner of shares of the Company with a value in excess of $25,000, and has held these shares continuously for at least one year.

Proposal Six - Shareholder Right to Call for a Special Shareholder Meeting

“Shareholders ask our board to take the steps necessary to amend the appropriate company governing documents to give the owners of a combined 10% of our outstanding common stock the power to call a special shareholder meeting.”

SUPPORTING STATEMENT SUBMITTED BY MR. GOLDSTEIN

Many companies provide for both a shareholder right to call a special shareholder meeting and a shareholder right to act by written consent. We have neither right.

A special shareholder meeting can be a means to elect a new director who is more qualified than a current director. For instance a majority of shares voted against Dana McGinnis at our 2021 annual meeting.

Please vote yes:

Shareholder Right to Call for a Special Shareholder Meeting - Proposal Six

Statement in Opposition to Proposal Six

The Board recommends a vote AGAINST this stockholder proposal, for the reasons set forth below.

A special meeting right at a 10% ownership threshold, as presented by this stockholder proposal, may shift power to a small group of stockholders, enable abuse and corporate waste.

The Company’s Amended and Restated Certificate of Incorporation and Amended and Restated Bylaws provide that the Board may call special meetings. The Board believes this approach gives the Company flexibility to call special stockholder meetings when members of the Board, acting as a fiduciaries, determine that a special meeting would be in the best interests of the Company’s stockholders.

Permitting stockholders holding only 10% of the Company’s outstanding stock to call special meetings, as requested by the proponent, would present a risk to the Company that a small group of self-interested stockholders could be given disproportionate amount of influence over the Company’s affairs. This would allow such stockholders to apply undue pressure or advance narrow purposes rather than those of the Company and our stockholder base as a whole.

27

Further, special meetings of stockholders can be potentially disruptive to business operations and can cause the Company to incur substantial expenses. Our Board members, management and employees must devote a significant amount of time and attention to preparing for a special meeting, which detracts from their primary focus of operating our business in the best interests of stockholders. In addition, with each special meeting, we must incur significant expenses in order to prepare the required disclosures, print and distribute materials, solicit proxies and tabulate votes. Accordingly, the Board believes that special meetings of the stockholders should be extraordinary events that are supported by the Board. Further, the proposed 10% threshold for a special meeting right is lower than the majority of S&P 500 or S&P Midcap 400 companies that offer stockholders the right to call special meetings and would be extremely uncommon for companies with a stockholder bases comparable to the Company. The Board believes that leaving the ability to call special meetings with the Board appropriately safeguards stockholder interests and prevents corporate waste.

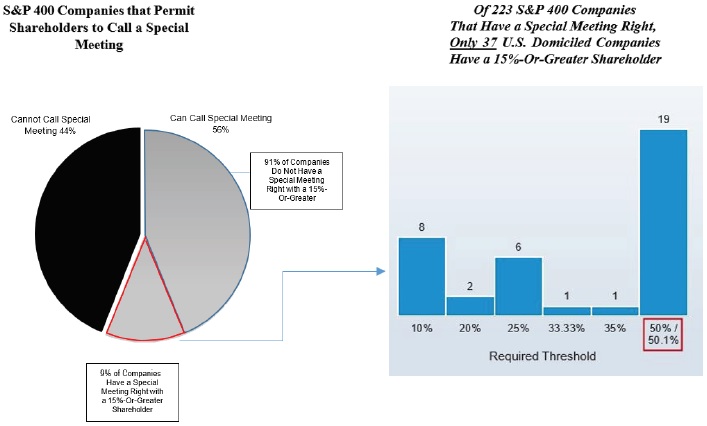

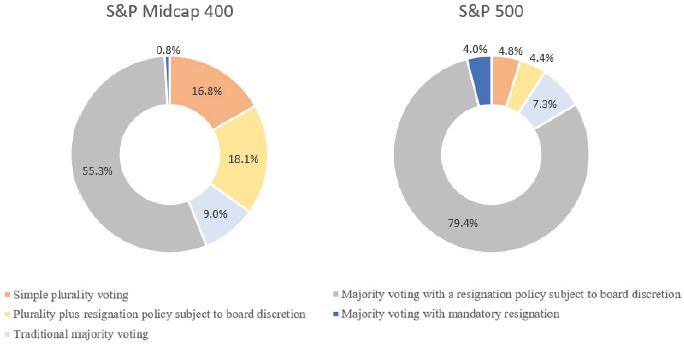

In making its recommendation, the Board reviewed data on public companies that allow stockholders to call special meetings and, in particular, those companies with a stockholder base comparable to the Company. As shown on the table below, of S&P Midcap 400 companies, 56% allow stockholders to call special meetings without Board approval and the majority of those that had a 15% or greater stockholder had special meeting thresholds of 50% or greater.

Source: DealPoint, September 13, 2022; and S&P Capital IQ, September 13, 2022

| 28 |

The proposal is unnecessary given the Company’s robust corporate governance practices and established engagement with and responsiveness to stockholders.

The Company already has numerous policies and mechanisms in place that enhance independent leadership, protect stockholders’ interests and allow for stockholders to inform the Board of concerns other than through a special meeting, including:

| · | The Co-Chairs of the Board are independent; | |

| · | Nine of the ten Board members are independent; | |

| · | All Board committees consist entirely of independent directors; | |

| · | Board members are limited to a term of 12 years; | |

| · | If Proposal Three is approved by stockholders, all Board members will be elected annually beginning in 2025; | |

| · | The Company has a majority voting standard for uncontested director elections and a director resignation policy; | |

| · | The Board is committed to meaningful engagement with stockholders and welcomes input and suggestions; | |

| · | The Company has adopted stock ownership guidelines for executive officers and directors; and | |

| · | The Board has adopted limits on the number of outside public company boards permitted for directors. |

All of the above corporate governance practices afford stockholders the ability to hold directors accountable.

Accordingly, for the foregoing reasons, the Board of Directors recommends a vote AGAINST this stockholder proposal.

THE BOARD OF DIRECTORS RECOMMENDS A VOTE “AGAINST” APPROVAL OF THE NON-BINDING STOCKHOLDER PROPOSAL FOR STOCKHOLDERS’ RIGHT TO CALL FOR A SPECIAL STOCKHOLDER MEETING.

| 29 |

PROPOSAL SEVEN

STOCKHOLDER PROPOSAL REGARDING HIRING AN INVESTMENT BANKER IN CONNECTION WITH THE EVALUATION OF A POTENTIAL SPINOFF

The following proposal was submitted by Kenneth Steiner, a stockholder of the Company. Mr. Steiner has informed the Company that he has held at least 10 shares of the Company continuously for at least two years.

Proposal Seven – Hire Investment Banker Regarding Potential Spinoff

“RESOLVED: The stockholders request that an investment banking firm be engaged to assess the profitability of the Company’s Water Services and Operations business and to evaluate alternatives to maximize its value including spinning it off to stockholders including a spinoff.”

SUPPORTING STATEMENT SUBMITTED BY MR. STEINER

Historically, the Company’s business model relied on royalties and fixed fees for the use of its land by oil and gas producers. That model required minimal capital and operating expenses. As a result, the Company’s profit margin was consistently greater than 90%.