UNITED

STATES

SECURITIES

AND EXCHANGE COMMISSION

Washington,

D.C. 20549

FORM

8-K

CURRENT

REPORT

Pursuant

to Section 13 or 15(d) of the Securities Exchange Act of 1934

Date of

Report (Date of earliest event reported): March 30, 2009

OPTEX SYSTEMS HOLDINGS,

INC.

(Exact

Name of Registrant as Specified in Charter)

|

Delaware

|

333-143215

|

33-143215

|

||

|

(State

or other jurisdiction of incorporation)

|

(Commission

File Number)

|

(IRS

Employer Identification No.)

|

|

1420 Presidential Drive, Richardson,

TX

|

75081-2439

|

|

|

(Address

of principal executive offices)

|

(Zip

Code)

|

Registrant’s telephone number,

including area code: 972-238-1403

|

Sustut

Exploration, Inc. 1420 5th Avenue #220

Seattle,

Washington 98101

|

|

(Former

name or former address, if changed since last

report)

|

Check the

appropriate box below if the Form 8-K filing is intended to simultaneously

satisfy the filing obligation of the registrant under any of the following

provisions:

o

Written communications pursuant to Rule 425 under the Securities Act (17 CFR

230.425)

o

Soliciting material pursuant to Rule 14a-12 under the Exchange Act (17 DFR

240.14a-12)

o

Pre-commencement communications pursuant to Rule 14d-2(b) under the Exchange Act

(17 CFR 240.14d-2(b))

o

Pre-commencement communications pursuant to Rule 13e-4 (c) under the Exchange

Act (17 CFR 240.13e-4(c))

ITEM

1.01 Entry into Material Definitive Agreement.

On March

30, 2009, Optex Systems Holdings, Inc. (formerly known as Sustut Exploration,

Inc., and the name was changed on March 26, 2009 pursuant to an amendment to the

Articles of Incorporation, filed with the State of Delaware) (the

“Registrant”) entered into an Agreement and Plan of Reorganization (the

“Reorganization Agreement”) with Optex Systems, Inc., a privately-held Delaware

corporation (“Optex”).

Closing

under the Reorganization Agreement was contingent, among other things, upon

receipt by the Registrant of (i) financial statements of Optex which have been

audited in accordance with generally accepted accounting principles in the U.S,

(ii) written approval from all shareholders of Optex of the terms of

Reorganization Agreement, (iii) receipt of representations from the

shareholders of Optex regarding their ownership of the shares and authority to

transfer them under the terms of the Reorganization Agreement free and clear of

any liens, claims or encumbrances, and (iv) delivery of the share certificates

representing all of the issued and outstanding stock of Optex, duly endorsed for

transfer. The parties closed the transaction on or about March 30,

2009.

Registrant,

Shareholders and Optex entered into this Agreement which provides, among other

things, that (i) the outstanding 85,000,000 shares of Optex Common Stock be

exchanged by Registrant for 113,333,282 shares of Registrant

Common Stock, (ii) the outstanding 1,027 shares of Optex Series A Preferred

Stock be exchanged by Registrant for 1,027 shares of Registrant Series A

Preferred Stock and such additional items as more fully described in the

Agreement and (iii) the 8,131,667 shares of Optex purchased in the private

placement were exchanged by Registrant for 8,131,667 shares of Registrant Common

Stock, as acknowledged by Registrant. Accordingly, following closing,

Optex will be a wholly-owned subsidiary of the Registrant, and the Registrant

will have a total of approximately 141,464,940 million common stock shares

issued and outstanding, of which 19,999,991 million will be owned by persons who

were previously shareholders of the Registrant and 121,464,949 will be owned by

persons who were previously shareholders of Optex, and/or their nominees.

Registrant will also have 1,027 shares of its Series A Preferred Stock

outstanding which will be owned by persons who were previously creditors of

Optex.

In

addition, pursuant to the terms and conditions of the Reorganization Agreement

upon Closing:

|

-

|

The

Registrant’s board of directors will be reconstituted to consist initially

of Stanley Hirschman, Merrick Okamoto and Ronald Richards.

|

|

-

|

All

current officers of the Registrant shall resign and the newly constituted

board of directors shall appoint Stanley Hirschman as President, and shall

appoint such other officers as it deems necessary and in the best

interests of the Registrant.

|

|

-

|

Following

closing, the Registrant shall complete the sale, transfer or other

disposition of its pre-closing business operations, including all assets

and liabilities related to such

operations.

|

Item

2.01 Completion of Acquisition or Disposition of Assets .

As used

in this Current Report on Form 8-K, all references to the “Company,” “we,” “our”

and “us” for periods prior to the closing of the Reorganization refer to the

Registrant, and for periods subsequent to the closing of the Reorganization

refer to the Registrant and its subsidiaries.

Information

regarding the Company, Optex and the principal terms of the Reorganization are

set forth below.

The

Reorganization

The Reorganization. On March

30, 2009, a closing occurred whereby the then existing shareholders of Optex

exchanged their shares of Optex Common Stock for the shares of Common Stock of

Registrant as follows: (i) the outstanding 85,000,000 shares of Optex

Common Stock were exchanged by Registrant for 113,333,282 shares of Registrant

Common Stock, (ii) the outstanding 1,027 shares of Optex Series A Preferred

Stock were exchanged by Registrant for 1,027 shares of Registrant Series A

Preferred Stock and such additional items as more fully described in the

Agreement and (iii) the 8,131,667 shares of Optex Common Stock purchased in the

private placement will be exchanged by Registrant for 8,131,667 shares of

Registrant Common Stock, as acknowledged by Registrant. Optex shall remain a

wholly owned subsidiary of Registrant, and Optex shareholders are now

shareholders of Registrant.

Simultaneously

with closing of the Reorganization Agreement (and the shares are included

above), as of March 30, 2009, Optex accepted subscriptions (“Private Placement”)

from accredited investors for a total 27 units (the "Units"), for $45,000 per

Unit, with each Unit consisting of Three Hundred Thousand (300,000) shares of

common stock, no par value (the "Common Stock") of Optex and warrants to

purchase Three Hundred Thousand (300,000) shares of Common Stock for $0.45 per

share for a period of five (5) years from the initial closing (the "Warrants"),

which were issued by Registrant after the closing referenced

above. Gross proceeds to the Company were $1,219,750, and after

deducting a finders fee of $139,555 which was payable in cash, and non-cash

consideration which constituted satisfaction of indebtedness owed to an investor

of $146,250, net proceeds were $933,945. The finder also received

five year warrants to purchase 2.7 Units, at an exercise price of $49,500 per

unit.

Neither

the Company nor Optex had any options or warrants to purchase shares of capital

stock outstanding immediately prior to or following the Reorganization, except

for 8,941,667 warrants issued in the Private Placement. Immediately prior the

the closing, Registrant adopted the 2009 Stock Option Plan providing for the

issuance of up to 6,000,000 shares for the purpose of having shares available

for the granting of options to Company officers, directors, employees and to

independent contractors who provide services to the Company.

The

shares of the Company’s common stock issued in connection with the

Reorganization and the private placement offering were not registered under the

Securities Act. All shares issued in connection with the Reorganization

were issued in reliance upon the exemption from registration provided by

Regulation D under the Securities Act, which exempts transactions to certain

accredited. The shares issued in connection with the private placement offering

were issued in part in reliance upon the exemption from registration provided by

Regulation D under the Securities Act and in part in reliance upon the exemption

from registration provided by Section 4(2) under the Securities Act for

transactions not involving any public offering. All such securities

constitute “restricted securities” as defined in Rule 144 under the Securities

Act of 1933, and may not be offered or sold in the United States absent

registration or an applicable exemption from the registration requirements.

Certificates representing these shares contain a restrictive legend stating the

same.

Changes Resulting from the

Reorganization. Registrant’s business is now the business of

Optex. Optex, which was founded in 1987, is a Richardson, Texas –

based ISO 9001:2000 certified concern, which manufactures optical sighting

systems and assemblies primarily for Department of Defense (DOD) applications.

Its products are installed on a majority of types of U.S. military land

vehicles, such as the Abrams and Bradley fighting vehicles, Light Armored and

Advanced Security Vehicles and have been selected for installation on the Future

Combat Systems (FCS) Stryker vehicle. Optex also manufactures and delivers

numerous periscope configurations, rifle and surveillance sights and night

vision optical assemblies. Optex delivers its products both directly to the

military services and to prime contractors. Optex

profitably delivers high volume products, under multi-year contracts, to large

defense contractors. Optex has the reputation and credibility with those

customers as a strategic supplier.

Following

completion of the Reorganization, the Company intends to carry on Optex’s

business as its sole line of business. The Company has relocated its executive

offices to Optex Systems, Inc., 1420 Presidential Drive, Richardson,

TX 75081-2439, and its telephone number is (972) 238-1403.

Changes to the Board of Directors.

In conjunction with closing under the terms of the Reorganization

Agreement, the number of members of the Company’s board of directors was

increased to three and Stanley Hirschman, Ronald Richards and Merrick Okamoto

were appointed to serve as Directors of the Company and Andrey Oks

resigned. Ronald Richards was appointed as Chairman of the

board of directors.

All of

the Company’s directors will hold office until the next annual meeting of the

stockholders or until the election and qualification of their successors. The

Company’s officers are elected by the board of directors and serve at the

discretion of the board of directors.

Name Change and Stock Option

Plan. On or about March 26, 2009, the Registrant’s board of

directors and shareholders approved the change of the Registrant’s name to

“Optex Systems Holdings, Inc.” and approved the 2009 Stock Option

Plan.

2009

Stock Option Plan. The purpose of the Plan is to to assist the

Registrant in attracting and retaining highly competent employees and to act as

an incentive in motivating selected officers and other employees of the

Registrant and its subsidiaries, and directors and consultants of the Registrant

and its subsidiaries, to achieve long-term corporate

objectives. There are 6,000,000 shares of common stock reserved for

issuance under this Plan. As of March 31, 2009, the Registrant had

not issued any stock options under this Plan.

Description

of the Business

Background

On March

30, 2009, a closing occurred whereby the then existing shareholders of the

Company exchanged their shares of Company Common Stock with the shares of Common

Stock of Sustut Exploration, Inc. (“Registrant”) as follows: (i) the

outstanding 85,000,000 shares of Company Common Stock were exchanged by

Registrant for 113,333,282 shares of Registrant Common Stock, (ii) the

outstanding 1,027 shares of Company Series A Preferred Stock were exchanged by

Registrant for 1,027 shares of Registrant Series A Preferred Stock and such

additional items as more fully described in the Agreement and (iii) the

8,131,667 shares of Company purchased in the private placement will be exchanged

by Registrant for 8,131,667 shares of Registrant Common Stock, as acknowledged

by Registrant. The

Company shall remain a wholly-owned subsidiary of Registrant, and the Company’s

shareholders are now shareholders of Registrant.

Simultaneously

with closing under the Reorganization Agreement (and the shares are included

above), as of March 30, 2009 , the Company accepted subscriptions (“Private

Placement”) from accredited investors for a total 27 units (the "Units"), for

$45,000.00 per Unit, with each Unit consisting of Three Hundred Thousand

(300,000) shares of common stock, no par value (the "Common Stock") of the

Company and warrants to purchase Three Hundred Thousand (300,000) shares of

Common Stock for $0.45 per share for a period of five (5) years from the initial

closing (the "Warrants"), which were issued by Registrant after the closing

referenced above. Gross proceeds to the Company were $1,219,750, and

after deducting a finders fee of $139,555 which was payable in cash, and

consideration which constituted of satisfaction of indebtedness owed to an

investor of $146,250, net proceeds were $933,945. The finder also

received five year warrants to purchase 2.7 Units, at an exercise price of

$49,500 per unit.

Optex,

which was founded in 1987, is a Richardson, Texas – based ISO 9001:2000

certified concern, which manufactures optical sighting systems and assemblies

primarily for Department of Defense (DOD) applications. Its products are

installed on a majority of types of U.S. military land vehicles, such as the

Abrams and Bradley fighting vehicles, Light Armored and Armored Security

Vehicles and have been selected for installation on the Future Combat Systems

(FCS) Stryker vehicle. Optex also manufactures and delivers numerous periscope

configurations, rifle and surveillance sights and night vision optical

assemblies. Optex delivers its products both directly to the military services

and to prime contractors.

Optex

profitably delivers high volume products, under multi-year contracts, to large

defense contractors. Optex has the reputation and credibility with those

customers as a strategic supplier. The successful completion of the separation

from IRSN has enhanced the Company’s ability to serve its existing customers and

will set the stage for it to become a center of manufacturing excellence. The

Company also anticipates the opportunity to integrate some of its night vision

and optical sights products into retail applications. The Company now

plans to carry on the business of Optex as its sole line of business, and all of

the Company’s operations are expected to be conducted by and through Optex.

All references to the “Company,” “we,” “our” and “us” for periods prior to

the closing of the Reorganization refer to the Registrant, and references to the

“Company,” “we,” “our” and “us” for periods subsequent to the closing of the

Reorganization refer to the Registrant and its subsidiaries.

Organizational

History

Optex

Systems, Inc., which was founded in 1987, is an ISO 9001:2000 certified concern

which manufactures optical sighting systems and assemblies primarily for

Department of Defense (DOD) applications. Optex was a privately-held company

since inception until being acquired by publicly traded Irvine Sensors Corp.

(IRSN) on December 30, 2005 and was operated as a wholly owned subsidiary of

IRSN. On October 14, 2008, Optex Systems Inc. (Delaware) acquired Optex Systems

in a public auction process. Optex Delaware was formed by the Longview Fund, LP

and Alpha Capital Antstalt, former secured creditors of IRSN, to consummate the

transaction with the Company, and subsequently, on February 20, 2009, Longview

Fund conveyed its ownership interest in the Company to Sileas Corp., an entity

owned by three of the Company’s officers.

Products

Optex

products are installed on a majority of types of U.S. military land vehicles,

such as the Abrams and Bradley fighting vehicles, Light Armored and Advanced

Security Vehicles and have been selected for installation on the Future Combat

Systems (FCS) Stryker vehicle. Optex also manufactures and delivers numerous

periscope configurations, rifle and surveillance sights and night vision optical

assemblies. Optex delivers its products both directly to the military services

and to prime contractors.

Optex

profitably delivers high volume products, under multi-year contracts, to large

defense contractors. Optex has the reputation and credibility with those

customers as a strategic supplier. The successful completion of the separation

from IRSN has enhanced the company’s ability to serve its existing customers and

will set the stage for it to become a center of manufacturing excellence. The

Company also anticipates the opportunity to integrate some of its night vision

and optical sights products into retail applications.

Specific

product lines include:

|

|

·

|

Electronic

sighting systems

|

|

|

·

|

Mechanical

sighting systems

|

|

|

·

|

Laser

protected glass periscopes

|

|

|

·

|

Laser

protected plastic periscopes

|

|

|

·

|

Non-laser

protected plastic periscopes

|

|

|

·

|

Howitzer

sighting systems

|

|

|

·

|

Ship

binoculars

|

|

|

·

|

Replacement

optics (e.g. filters, mirrors)

|

Location and

Facility

Optex is

located in Richardson, TX in a 49,000 square foot facility and currently has 109

employees. The Company operates with a single shift, and capacity could be

expanded by adding a second shift. The Company’s proprietary

processes and methodologies serve to provide barriers to entry by other

competing suppliers. In many cases Optex is the sole source provider or one of

only two providers of a product. It has capabilities which include

machining, bonding, painting, tracking, engraving and assembly and can perform

both optical and environmental testing in-house.

Prior Operational/Financial

Challenges; Recovery; and Future Growth Potential

During

the IRSN phase of Optex’s history, its parent company faced certain business

challenges and utilized the cash flow from Optex to meet other non-Optex

needs. This left Optex with inadequate operating

resources.

Since the

buyout, the Optex picture has dramatically changed. Management has

made substantial progress in increasing operational efficiencies and

productivity and has become profitable. Based on this progress,

management estimates 2009 annual revenue of $27.4 million to be drawn from its

$42 million backlog and ongoing contractual business.

Optex is

currently bidding on several substantial government contracts to expand sales

and production beyond the current production and backlog. It is also

exploring possibilities to adapt some of its products for commercial use where

those markets show potential for solid revenue growth.

Market Opportunity – U.S.

Military

Optex

products are currently marketed in the military and related government

markets. Since 1998, American military spending has increased over

225% on an annual basis to over $600 billion per year. As the

American presence overseas continues, this level of spending should continue to

exist. Also, the market for replacement parts for existing military

equipment is significant.

Optex

meets the U.S. military requirements in its product lines:

|

|

·

|

Reliability

– failure can cost lives

|

|

|

·

|

Cost

effectiveness

|

|

|

·

|

Ability

to deliver on schedule

|

|

|

·

|

Armed

forces need to be able to see to

perform

|

|

|

·

|

Mission

critical products.

|

Therefore,

Optex is well positioned to continue to service U.S. military

needs.

Market Opportunity –

Commercial/Retail

Optex

products are currently sold exclusively to military and related government

markets. We believe we have significant potential retail opportunities to

commercialize various products we presently manufacture. Our initial

focus will be directed in three product areas.

|

|

·

|

Big

Eye Binoculars – While the military application we produce is based on

mature military designs, Optex owns all castings, tooling and glass

technology. These large fixed mount binoculars could be sold to

Cruise Ships, Personal Yachts and

Cities/Municipalities.

|

|

|

·

|

Night

Vision Goggles – Optex presently manufactures the Optical System for the

NL-61 Night Vision Goggles for the Ministry of Defense of Israel. This

technology is based on the IR Squared design and could be implemented for

retail commercial applications.

|

|

|

·

|

Infrared

Imaging Equipment – Optex manufactures and assembles Infrared Imaging

Equipment for Textron and components for Raytheon’s Thermal Imaging M36

Mount product. This equipment and technology has potential to be assembled

for border patrol, police and security

agencies.

|

Customer

Base

Optex

serves customers in three primary categories: as prime contractor

(TACOM, U.S. Army, Navy and Marine Corps), as subcontractor (General Dynamics,

BAE, Raytheon and Northrop) and also as a supplier to foreign governments

(Israel, Australia and NAMSA). Although we do serve all three of

these categories, at present, approximately 90% of the gross revenue from our

business is derived from two customers, General Dynamics Land Systems (“GDLS”)

and U.S. Army TACOM, with which we have approximately 50 discrete contracts

which cover supply of all of vehicles, product lines and spare

parts. Given the size of GDLS and TACOM as well as the fact that the

contracts are not interdependent, we are of the opinion that this provides us

with a well diversified customer pool. This broad base enables Optex

to mitigate its risk in this economic environment by not relying on a sole or

few sources of revenue as well as providing a broad base from which to build its

future business.

Marketing

Plan

Optex has

used two models to help define its Marketing Plan. First, Michael

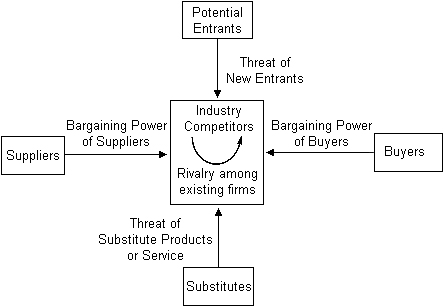

Porter’s Five Force Model.

Potential Entrants –

Low. In order to enter this market companies have a large

barrier to entry. The first hurdle is that an entrant would need to

prove the existence of a government approved accounting systems for larger

contracts. Second, the entrant would need to develop the processes

required to produce the product. Third, the entrant would need to

produce product and submit successful test requirements (many of which need

government consultation to complete). Finally, in many cases the

customer has an immediate need, cannot wait for this qualification cycle, and

must issue the contracts to existing suppliers.

Buyers –

Medium. In most cases the buyers have two fairly strong

suppliers. It is in their best interest to keep at least two, and

therefore in some cases the contracts are split between suppliers. In

the case of larger contracts, the customer can potentially request an open book

policy on costs and expect a reasonable margin has been applied.

Substitutes –

Low. Optex has both new vehicle contracts and replacement part

contracts for the exact same product. The US Government has declared

that the Abrams/Bradley base vehicles will be the ground vehicle of choice out

through 2040. This allows efficiencies within the supply chain and a

very long ROI on new vehicle proposals.

Suppliers – Low to

Medium. The suppliers of standard processes (casting,

machining, plating, etc.) have very little power. Given the current

state of the economy, they need to be very competitive to gain and /or maintain

contracts. Those suppliers of products which use Top Secret Clearance

processes are slightly better off; however, there continues to be multiple

avenues of supply and therefore moderate power.

Industry Competitors –

Low. The current suppliers have been partitioned according to

their processes and the products. Optex and Miller-Holzwarth tend to

compete for the plastic periscope products whereas Optex and Seiler have

competed on the higher level products. In the last 12-18 months,

Optex has begun to challenge Seiler in areas where they have long held the

dominant role. For example, while the existing Howitzer contracts are

at low margins, the new bids will be at a much higher margin now that Optex has

proven they can produce the product.

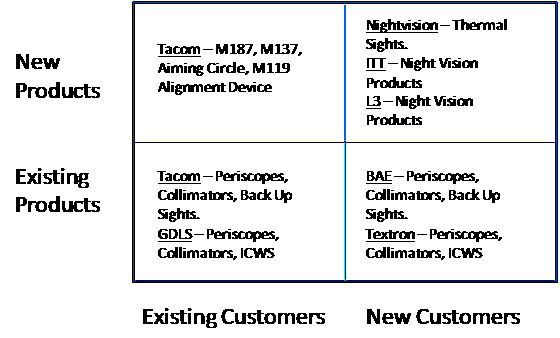

The

second model is a two by two matrix for Products and Customers.

This

model describes three basic actions for Optex:

|

|

1)

|

Take

Existing Products into the applications of New

Customers.

|

|

|

2)

|

Take

New Products into our Existing

Customers.

|

|

|

3)

|

Expand

the Portfolio by developing New Products for New

Customers.

|

Operations

Plan

The

Operations Plan for Optex can be broken down into three distinct

areas: Material Management, Manufacturing Space Planning, and

Efficient Economies of Scale.

Materials

Management

The

largest portion of costs captured in the Optex Income Statement is

Materials. Optex has completed the following activities in order to

demonstrate continuous improvement:

|

|

-

|

Successful

Completion of ISO9001:2000

Re-Certification

|

|

|

-

|

Weekly

Cycle Counts on Inventory Items

|

|

|

-

|

Weekly

Material Review Board Meeting on non-moving piece

parts

|

|

|

-

|

Kanban

kitting on products with consistent weekly ship

quantities

|

|

|

-

|

Daily

review of Yields and Product

Velocity

|

|

|

-

|

Bill

of Material Reviews prior to Work Order

Release

|

Future

continuous improvement opportunities include installation and training of the

Shop Floor Control module within our ERP system and organizational efficiencies

of common procurement techniques among buyers.

Manufacturing Space

Planning

The

existing square footage occupied by Optex is 49,000. While not

critical at this time, Optex needs to explore expansion opportunities to support

future growth. Given the ample building opportunities along with

competitive lease rates, the objective is to maintain building and building

related costs consistent on a percent to sales perspective on the Income

Statement. This leads to the third and final area.

Efficient Economies of

Scale

Consistent

with the aforementioned Space Planning, Optex will drive the economies of scale

to reduce support costs on a percentage of sales basis. These cost

reductions can then be either brought directly to the bottom line or used for

business investment.

This

process is driven by the use of Six Sigma techniques and Process

Standardization. Initial activities in this area have been the

success of 5S projects in several production areas which has lead to improved

output and customer approval on the aesthetics of the work

environment. In addition to the 5S projects, Optex has used the DMAIC

(Define, Measure, Analyze, Improve, Control) Problem Solving technique to

identify bottlenecks within the process flow and improve product

yields. These successful techniques can then be duplicated across the

production floor and drive operational improvements.

Intellectual

Property

We

utilize several highly specialized and unique processes in the manufacture of

our products. While we believe that these trade secrets have value,

it is probable that our future success will depend primarily on the innovation,

technical expertise, manufacturing and marketing abilities of our personnel. We

cannot assure you that we will be able to maintain the confidentiality of our

trade secrets or that our non-disclosure agreements will provide meaningful

protection of our trade secrets, know-how or other proprietary information in

the event of any unauthorized use, misappropriation or other

disclosure. The confidentiality agreements that are designed to

protect our trade secrets could be breached, and we might not have adequate

remedies for the breach. Additionally, our trade secrets and

proprietary know-how might otherwise become known or be independently discovered

by others. We do not possess any patents.

Our

competitors, many of which have substantially greater resources, may have

applied for or obtained, or may in the future apply for and obtain, patents that

will prevent, limit or interfere with our ability to make and sell some of our

products. Although we believe that our products do not infringe on the patents

or other proprietary rights of third parties, we cannot assure you that third

parties will not assert infringement claims against us or that such claims will

not be successful.

Competition

The

markets for our products are competitive. We compete primarily on the basis of

our ability to design and engineer products to meet performance specifications

set by our customers. Our customers include the military and government end

users as well as prime contractors that purchase component parts or

subassemblies, which they incorporate into their end

products. Product pricing, quality, customer support, experience,

reputation and financial stability are also important competitive

factors.

There are

a limited number of competitors in each of the markets for the various types of

products that we design, manufacture and sell. At this time we consider our

primary competitors to be Seiler Instruments, Miller-Holzwarth, Kent Periscopes,

and EO System Co.

Our

competitors are often well entrenched, particularly in the defense markets. Some

of these competitors have substantially greater resources than we do. While we

believe that the quality of our technologies and product offerings provides us

with a competitive advantage over certain manufacturers, some of our competitors

have significantly more financial and other resources than we do to spend on the

research and development of their technologies and for funding the construction

and operation of commercial scale plants.

We expect

our competitors to continue to improve the design and performance of their

products. We cannot assure investors that our competitors will not develop

enhancements to, or future generations of, competitive products that will offer

superior price or performance features, or that new technology or processes will

not emerge that render our products less competitive or obsolete. Increased

competitive pressure could lead to lower prices for our products, thereby

adversely affecting our business, financial condition and results of operations.

Also, competitive pressures may force us to implement new technologies at a

substantial cost, and we may not be able to successfully develop or expend the

financial resources necessary to acquire new technology. We cannot assure you

that we will be able to compete successfully in the future.

External Growth

Potential/Roll-Up Opportunities

Optex

operates in a business environment which is highly fragmented with numerous

private companies which were established more than 20 years ago. Some of these

companies were founded by family members 2-3 generations before the present

family operators. Optex believes there are opportunities to seek

mergers of strategic competitors once we are a public entity. We are not aware

of any previous attempts to roll-up companies with our defense manufacturing

expertise.

The

typical company we compete with has 50-100 employees and annual revenue of

$20-$50 million dollars. Most of these private companies have never had the

opportunity to enjoy the benefits of consolidation and the resulting economies

of scale which this can provide.

We plan

to engage our competition on a selective basis, and explore all opportunities to

grow our operations through mergers and/or acquisitions.

We have

no acquisition agreements pending at this time and are not currently in

discussions or negotiations with any third parties.

Employees

The

Company has 109 employees. To the best of its knowledge, the Company is

compliant with local prevailing wage, contractor licensing and insurance

regulations, and has good relations with its employees.

Forward-Looking

Statements

This

Current Report on Form 8-K contains forward-looking statements. To the extent

that any statements made in this Current Report on Form 8-K contain information

that is not historical, these statements are essentially forward-looking.

Forward-looking statements can be identified by the use of words such as

“expects,” “plans,” “will,” “may,” “anticipates,” believes,” “should,”

“intends,” “estimates,” and other words of similar meaning. These statements are

subject to risks and uncertainties that cannot be predicted or quantified and,

consequently, actual results may differ materially from those expressed or

implied by such forward-looking statements. Such risks and uncertainties are

outlined in “Risk Factors” and include, without limitation, the Company’s

ability to raise additional capital to finance the Company’s activities; the

effectiveness, profitability, and the marketability of its products; legal and

regulatory risks associated with the Reorganization ; the future trading of the

common stock of the Company; the ability of the Company to operate as a public

company; the period of time for which the proceeds of the Private Placement will

enable the Company to fund its operations; the Company’s ability to protect its

proprietary information; general economic and business conditions; the

volatility of the Company’s operating results and financial condition; the

Company’s ability to attract or retain qualified senior management personnel and

research and development staff; and other risks detailed from time to time in

the Company’s filings with the SEC, or otherwise.

Information

regarding market and industry statistics contained in this Report is included

based on information available to the Company that it believes is accurate. It

is generally based on industry and other publications that are not produced for

purposes of securities offerings or economic analysis. The Company has not

reviewed or included data from all sources, and cannot assure investors of the

accuracy or completeness of the data included in this Report. Forecasts and

other forward-looking information obtained from these sources are subject to the

same qualifications and the additional uncertainties accompanying any estimates

of future market size, revenue and market acceptance of products and services.

The Company does not undertake any obligation to publicly update any

forward-looking statements. As a result, investors should not place undue

reliance on these forward-looking statements.

Management’s

Discussion and Analysis or Plan of Operations

All

references to the “Company,” “we,” “our” and “us” for periods prior to the

closing of the Reorganization refer to Optex, and references to the “Company,”

“we,” “our” and “us” for periods subsequent to the closing of the Reorganization

refer to the Registrant and its subsidiaries.

The

following discussion highlights the principal factors that have affected our

financial condition and results of operations as well as our liquidity and

capital resources for the periods described. This discussion contains

forward-looking statements. Please see “Special cautionary statement concerning

forward-looking statements” and “Risk factors” for a discussion of the

uncertainties, risks and assumptions associated with these forward-looking

statements. The operating results for the periods presented were not

significantly affected by inflation.

Plan

of Operation

Through a

private placement offering completed in conjunction with closing under the

Reorganization Agreement, the Company has raised $1,219,750 ($933,945, net of

finders fees and satisfaction of indebtedness owed to an investor) to fund

operations. The proceeds will be used as follows:

|

Description

|

Offering

|

|||

|

Additional

Personnel

|

$ | 150,000 | ||

|

Legal

and Accounting Fees

|

$ | 100,000 | ||

|

Working

Capital

|

$ | 683,945 | ||

|

Totals:

|

$ | 933,945 | ||

Results

of Operations

Three

Months Ended December 31, 2008 Compared to the Three Months Ended December,

2007

Revenues. During

the three months ended December 28, 2008, we recorded revenues of $7.2 million,

as compared to revenue for the three months ended December 30, 2007 of $4.4

million, an increase of $2.9 million or 64.5%. This increase in

revenues was primarily due to the ramp up of production on our U.S. government

and General Dynamics periscope lines to meet new orders and accelerated delivery

customer requirements..

Cost of Goods

Sold. During the quarter ended December 28, 2008, we recorded

cost of goods sold of $6.3 million as opposed to $3.8 million during the quarter

ended December 30, 2007, an increase of $2.5 million or 64.2%. This

increase in cost of goods sold was primarily due to increased revenue on our

periscope lines in support of higher backlog and accelerated delivery

schedules.

G&A Expenses. During the

three months ended December 28, 2008, we recorded operating expenses of $ 0.6

million as opposed to $1.2 million during the three months ended December 30,

2007, a decrease of $0.6 million or 50%. This decrease in G&A

expenses was primarily due to the elimination of Corporate Cost allocations from

Irvine Sensors of $0.4 million, the Irvine Sensors, Employee Stock Bonus Plan

(ESBP) of $0.1 million and further reductions in consulting and travel expenses

previously charged to Optex by Irvine Sensors in the three months ended December

30, 2007.

Earnings Before Other Expenses and

Taxes. During the three months ended December 28, 2008, we recorded

earnings of $0.3 million as opposed to $(0.6 million) during the three months

ended December 30, 2007, an increase of 0.9 million or 150%. This

increase in earnings before other expenses and taxes was primarily due to

increased sales revenue in the three months ended December 28, 2008 combined

with reduced general and administrative expenses driven by the elimination of

Irvine Sensors corporate costs pushed down to Optex in the three months ended

December 30, 2007.

Net Loss. During

the three months ended December 28, 2008, we recorded a net loss of $0.03

million, as compared to $0.69 million for three months ended December 30, 2007,

a decrease of $0.7 million or 97.1%. This decrease in net loss was

principally the result of an reduction in operating expenses related to costs

pushed down from Irvine Sensors in the three months ended December 30, 2007

combined with increased revenue in three months ended December 28,

2008. Additionally, in the three months ended December 28, 2008 Optex

incurred $0.5 million in intangible expenses, representing an increase of $0.3

million over the three months ended December 30, 2007. The increased

intangible expenses relate to the acquisition of Optex from Irvine

Sensors.

Year

Ended September 28, 2008 Compared to Year Ended September 30, 2007

Revenues. During

the year ended September 28, 2008, we recorded revenues of $20.0 million, as

compared to revenue for the year ended September 30, 2007 of $15.4 million, an

increase of $4.6 million or 29.9%. This increase in revenues was

primarily due to increased shipments on the ICWS periscope, and M137 & M187

Howitzer programs.

Cost of Goods

Sold. During the year ended September 28, 2008, we recorded

cost of goods sold of $18.1 million as opposed to $17.4 million during the year

ended September 30, 2007, an increase of $0.7 million or 4.5%. This

increase in cost of goods sold was primarily due to increased revenues of $4.6

million. The margins on the increased revenue is significantly

improved over the year ended September 30, 2007 due to equitable price

adjustments and accelerated schedule consideration received in the year ended

September 2008 on periscopes and Howitzer programs. Additionally, the

gross margin for year ended September 30, 2007 included significant contract

loss reserves, excess and obsolescence and other non recurring inventory

adjustments related to unrecoverable costs increases on fixed price contracts

..

Loss Before Other Expenses and

Taxes. During the year ended September 28, 2008, we recorded a loss of

$3.1 million as opposed to $6.8 million during the year ended September 30,

2007, a decrease of $3.7 million or 54.4%. This decrease in loss was

primarily due to the negotiation of several equitable price adjustments and

consideration on accelerated delivery schedules in the year ended September 28,

2008. Additionally, for the year ended December 30, 2007

non recoverable cost increases on fixed price contracts resulted in significant

contract loss and excess and obsolete inventory reserves as discussed above in

cost of goods sold. These losses were partially offset in 2008 with

equitable price adjustments negotiated with the customer.

Net Loss. During

the year ended September 28, 2008, we recorded a net loss of $4.8 million, as

compared to $6.8 million for year ended September 30, 2007, a decrease of $2.0

million or 29.4%. This decrease in net loss was principally the

result of increased revenues and negotiated equitable and other price

adjustments discussed above partially offset by a $1.6 million adjustment for

asset impairment of goodwill, Goodwill was reviewed as of September

28, 2008 based upon the most recent value of the company as determined by the

sale to third party purchasers on October 14, 2008.

Liquidity

and Capital Resources

We have

historically met our liquidity requirements from a variety of sources, including

government and customer funding through contract progress bills, short term

loans, and notes from related parties. Based on our

strategy and the anticipated growth in our business, we believe that our

liquidity needs will increase. The amount of such increase will depend on many

factors, including the costs associated with the fulfillment of our projects,

whether we upgrade our technology, and the amount of inventory required for our

expanding business.

For

the 3 months ended December 28, 2008

Cash and Cash

Equivalents. As of December 28, 2008, we had cash and cash

equivalents of $0.5 million, as compared to cash and cash equivalents of $0.1

million as of December 30, 2007.

Net Cash Used in Operating

Activities. Net cash provided in operating activities totaled $0.5

million for the 3 months ended December 28, 2008, as compared to $0.3 million

used for the 3 months ended December 30, 2007.

Net Cash Used in Investing

Activities. Net cash used in investing activities totaled $0.02 million

during the 3 months ended December 28, 2008, as compared to net cash used in

investing activities of $0.03 million during the 3 months ended December 30,

2007.

Net Cash Provided By Financing

Activities. Net cash provided by financing activities totaled $0.2

million during the 3 months ended December 28, 2008, as compared to zero during

the 3 months ended December 30, 2007.

For

the 12 months ended September 28, 2008

Cash and Cash

Equivalents. As of September 28, 2008, we had cash and cash

equivalents of $0.2 million compared to $0.5 million in 2007.

Net Cash Used in Operating

Activities. For the year ended September 28, 2008 we used $0.6 million of

net cash in operating activities, as compared to using $1.5 million of net cash

in operating activities during 2007.

Net Cash Used in Investing

Activities. Net cash used in investing activities totaled $0.1 million

during the 12 months ended September 28, 2008, as compared to net cash used in

investing activities of $0.06 million during the 12 months ended September 30,

2007.

Net Cash Provided By Financing

Activities. Net cash provided by financing activities totaled $0.4

million during the 12 months ended September 28, 2008, as compared to net cash

provided by financing activities of $2.0 million during the 12 months

ended September 30, 2007

Critical

Accounting Policies and Estimates

Basis

of Presentation

The

accompanying financial statements include the historical accounts of Optex Texas

(hereinafter, the “Company” or “Optex Texas”). The financial statements have

been presented as subsidiary-only financial statements, reflecting the balance

sheets, results of operations and cash flows of the subsidiary as a stand-alone

entity.

Although,

the Company has been majority-owned by various parent companies, no accounts of

the parent companies or the effects of consolidation with any parent companies

have been included in the accompanying financial statements.

The

financial statements have been presented on the basis of push down

accounting in accordance with Staff Accounting Bulletin No. 54 (SAB

54) Application of

“Push Down” Basis of Accounting in Financial Statements of Subsidiaries Acquired

by Purchase. SAB 54 states that the push down basis of accounting should

be used in a purchase transaction in which the entity becomes wholly-owned.

Under the push down basis of accounting certain transactions incurred by the

parent company, which would otherwise be accounted for in the accounts of the

parent, are “pushed down” and recorded on the financial statements of the

subsidiary. Accordingly, items resulting from the purchase transaction such as

goodwill, debt incurred by the parent to acquire the subsidiary and other costs

related to the purchase have been recorded on the financial statements of the

Company.

Use of

Estimates: The preparation of

financial statements in conformity with accounting principles generally accepted

in the United States of America requires management to make estimates and

assumptions that affect reported amounts of assets and liabilities and

disclosure of contingent assets and liabilities at the date of the financial

statement and the reported amounts of revenues and expenses during the reporting

period. Actual results could differ from the estimates.

Accounts

Receivable: The Company records its accounts receivable at the original

sales invoice amount less shipment liquidations for previously collected

advance/progress bills and an allowance for doubtful accounts. An account

receivable is considered to be past due if any portion of the receivable balance

is outstanding beyond its scheduled due date. On a quarterly basis, the Company

evaluates its accounts receivable and establishes an allowance for doubtful

accounts, based on its history of past write-offs and collections, and current

credit conditions. No interest is accrued on past due accounts receivable. As

the customer base is primarily U.S. government and government prime contractors,

the Company has concluded that there is no need for an allowance for doubtful

accounts for the years ended September 28, 2008 and September 30,

2007.

Warranty

Costs: Optex warrants the quality of its products to meet

customer requirements and be free of defects for twelve months subsequent to

delivery. On certain product lines the warranty period has been

extended to 24 months due to technical considerations incurred during the

manufacture of such products. In the year ended September 28, 2008,

the company incurred $227,000 of warranty expenses representing the estimated

cost of repair or replacement for specific customer returned products still

covered under warranty as of the return date and awaiting replacement, in

addition to estimated future warranty costs for shipments occurring during the

twelve months proceeding September 28, 2008. Future warranty costs

were determined, based on estimated cost of replacement for expected returns

based upon our most recent experience rate of defects as a percentage of

sales. Prior to fiscal year 2008, all warranty expenses were incurred

as product was replaced with no reserve for warranties against deliveries in the

covered period.

Estimated Costs

to Complete and Accrued Loss on Contracts: The Company reviews

and reports on the performance of its contracts and production orders against

the respective resource plans for such contracts/orders. These reviews are

summarized in the form of estimates to complete ("ETC”s) and estimates at

completion (“EAC”s). EACs include Optex’s incurred costs to date

against the contract/order plus management's current estimates of remaining

amounts for direct labor, material, other direct costs and subcontract support

and indirect overhead costs based on the completion status and future

contractual requirements for each order. If an EAC indicates a potential overrun

(loss) against a fixed price contract/order, management generally seeks to

reduce costs and /or revise the program plan in a manner consistent with

customer objectives in order to eliminate or minimize any overrun and to secure

necessary customer agreement to proposed revisions.

If an EAC

indicates a potential overrun against budgeted resources for a fixed price

contract/order, management first attempts to implement lower cost solutions to

still profitably meet the requirements of the fixed price

contract. If such solutions do not appear practicable, management

makes a determination whether to seek renegotiation of contract or order

requirements from the customer. If neither cost reduction nor renegotiation

appears probable, an accrual for the contract loss/overrun is recorded against

earnings and the loss is recognized in the first period the loss is identified

based on the most recent EAC of the particular contract or product

order.

Goodwill and

Other Intangible Assets: Goodwill represents the cost of

acquired businesses in excess of fair value of the related net assets at

acquisition. The Company does not amortize goodwill, but tests it

annually for impairment using a fair value approach as of the first day of its

fourth fiscal quarter and between annual testing periods, if circumstances

warrant. Goodwill of Optex was reviewed as of September 30, 2007 and

based on the assessment, it was determined that no impairment was

required. Goodwill was reviewed as of September 28, 2008, and it was

determined that an impairment charge of $1,586,416 was required. The fair values

assigned to the assets of the Company and the goodwill was based upon the most

recent value of the Company as determined by the sale to third party purchasers

on October 14, 2008.

The

Company amortizes the cost of other intangibles over their estimated useful

lives, unless such lives are deemed indefinite. Amortizable intangible assets

are tested for impairment based on undiscounted cash flows and, if impaired,

written down to fair value based on either discounted cash flows or appraised

values. The identified amortizable intangible assets at September 28, 2008 and

September 30, 2007 derived from the acquisition of Optex by Irvine Sensors and

consisted of non-competition agreements and customer backlog, with initial

useful lives ranging from two to eight years. Intangible assets with indefinite

lives are tested annually for impairment, as of the first day of the Company's

fourth fiscal quarter and between annual periods, if impairment indicators

exist, and are written down to fair value as required.

Revenue

Recognition: The Company recognizes revenue upon transfer of title at the

time of shipment (F.O.B. shipping point), when all significant contractual

obligations have been satisfied, the price is fixed or determinable, and

collectability is reasonably assured.

Recent

Accounting Pronouncements

In June

2006, The FASB issued Interpretation No. 48 “Accounting for Uncertainty in Income

Taxes—an interpretation of FASB Statement No. 109” (“FIN 48”). This

Interpretation clarifies the accounting for uncertainty in income taxes

recognized in an enterprise’s financial statements in accordance with FASB No.

109, “Accounting for Income

Taxes”. FIN 48

prescribes a recognition threshold and measurement attribute for the financial

statement recognition and measurement of a tax position taken or expected to be

taken in a tax return. FIN 48 also provides guidance on de-recognition,

classification, interest and penalties, accounting in interim periods,

disclosure, and transition. FIN 48 is effective for fiscal years beginning after

December 15, 2006. The adoption of FIN 48 did not have a material impact on the

Company's consolidated financial position, results of operations, or cash

flows.

In

September 2006, the FASB issued FASB No. 157, “Fair Value Measurements”

which establishes a framework for measuring fair value, and expands disclosures

about fair value measurements. While FASB No. 157 does not apply to transactions

involving share-based payment covered by FASB No. 123, it establishes a

theoretical framework for analyzing fair value measurements that is absent from

FASB No. 123. We have relied on the theoretical framework established by FASB

No. 157 in connection with certain valuation measurements that were made in the

preparation of these financial statements. FASB No. 157 is effective for years

beginning after November 15, 2007. Subsequent to the Standard’s issuance, the

FASB issued an exposure draft that provides a one year deferral for

implementation of the Standard for non-financial assets and liabilities. The

Company is currently evaluating the impact FASB No. 157 will have on its

financial statements.

In

February 2007, Statement of Financial Accounting Standards No. 159, “The Fair Value Option for Financial

Assets and Financial Liabilities-Including an Amendment of FASB Statement No.

115,” (FASB 159), was issued. This standard allows a company to

irrevocably elect fair value as the initial and subsequent measurement attribute

for certain financial assets and financial liabilities on a contract-by-contract

basis, with changes in fair value recognized in earnings. The provisions of this

standard are effective as of the beginning of our fiscal year 2008, with early

adoption permitted. The Company is currently evaluating what effect the adoption

of FASB 159 will have on its financial statements.

In March

2007, the Financial Accounting Standards Board ratified Emerging Issues Task

Force (“EITF”) Issue No. 06-10, "Accounting for Collateral Assignment

Split-Dollar Life Insurance Agreements”. EITF 06-10 provides guidance

for determining a liability for the postretirement benefit obligation as well as

recognition and measurement of the associated asset on the basis of the terms of

the collateral assignment agreement. EITF 06-10 is effective for

fiscal years beginning after December 15, 2007. The Company is

currently evaluating the impact of EITF 06-10 on its financial statements, but

does not expect it to have a material effect.

In

December 2007, the FASB issued SFAS No. 141(R), Business Combinations and

SFAS No. 160, Accounting

and Reporting of Noncontrolling Interest in Consolidated Financial Statements,

an amendment of ARB No. 51. These new standards will significantly

change the accounting for and reporting of business combinations and

non-controlling (minority) interests in consolidated financial statements.

Statement Nos. 141(R) and 160 are required to be adopted simultaneously and

are effective for the first annual reporting period beginning on or after

December 15, 2008. Earlier adoption is prohibited. The Company is currently

evaluating the impact of adopting SFAS Nos. 141(R) and SFAS 160 on its

financial statements. See Note 14 to the financial statements for the year ended

September 28, 2008 for adoption of SFAS 141R subsequent to September 30,

2008.

In

December 2007, the SEC issued Staff Accounting Bulletin No. 110 (“SAB 110”). SAB

110 permits companies to continue to use the simplified method, under certain

circumstances, in estimating the expected term of “plain vanilla” options beyond

December 31, 2007. SAB 110 updates guidance provided in SAB 107 that previously

stated that the Staff would not expect a company to use the simplified method

for share option grants after December 31, 2007. The Company does not have any

outstanding stock options.

In March

2008, the Financial Accounting Standards Board (“FASB”) issued Statement of

Financial Accounting Standard (“SFAS”) No. 161, "Disclosures about Derivative

Instruments and Hedging Activities—an amendment of FASB Statement No.

133”. SFAS 161 requires enhanced disclosures about an entity’s

derivative and hedging activities. SFAS 161 is effective for

financial statements issued for fiscal years and interim periods beginning after

November 15, 2008 with early application encouraged. As such, the Company is

required to adopt these provisions at the beginning of the fiscal year

ended September

30, 2009.

The Company is currently evaluating the impact of SFAS 161 on its financial

statements but does not expect it to have a material effect

In May

2008, the Financial Accounting Standards Board issued Statement of Financial

Accounting Standard (“SFAS”) No. 162, "The Hierarchy of Generally Accepted

Accounting Principles”. SFAS 162 identifies the sources of

accounting principles and the framework for selecting the principles used in the

preparation of financial statements of nongovernmental entities that are

presented in conformity with generally accepted accounting principles (GAAP) in

the United States. SFAS 162 is effective 60 days following the SEC’s

approval of the Public Company Accounting Oversight Board amendments to AU

Section 411, The Meaning of Present Fairly in Conformity With Generally Accepted

Accounting Principles. The Company is currently evaluating the impact of SFAS

162 on its consolidated financial statements but does not expect it to have a

material effect.

In May

2008, the Financial Accounting Standards Board (“FASB”) issued Statement of

Financial Accounting Standard (“SFAS”) No. 163, "Accounting for Financial Guarantee

Insurance Contracts—an interpretation of FASB Statement No. 60" (“SFAS

163”). SFAS 163 interprets Statement 60 and amends existing

accounting pronouncements to clarify their application to the financial

guarantee insurance contracts included within the scope of that

Statement. SFAS 163 is effective for financial statements issued for

fiscal years beginning after December 15, 2008, and all interim periods within

those fiscal years. As such, the Company is required to adopt these

provisions at the beginning of the fiscal year ended September

30, 2011. The Company is currently evaluating the impact of SFAS 163

on its financial statements but does not expect it to have a material

effect.

Cautionary

Factors That May Affect Future Results

This

Current Report on Form 8-K and other written reports and oral statements made

from time to time by the Company may contain so-called “forward-looking

statements,” all of which are subject to risks and uncertainties. You can

identify these forward-looking statements by their use of words such as

“expects,” “plans,” “will,” “estimates,” “forecasts,” “projects” and other words

of similar meaning. You can identify them by the fact that they do not relate

strictly to historical or current facts. These statements are likely to address

the Company’s growth strategy, financial results and product and development

programs. You must carefully consider any such statement and should understand

that many factors could cause actual results to differ from the Company’s

forward-looking statements. These factors include inaccurate assumptions and a

broad variety of other risks and uncertainties, including some that are known

and some that are not. No forward-looking statement can be guaranteed and actual

future results may vary materially.

The

Company does not assume the obligation to update any forward-looking statement.

You should carefully evaluate such statements in light of factors described in

the Company’s filings with the SEC, especially on Forms 10-K, 10-Q and 8-K. In

various filings the Company has identified important factors that could cause

actual results to differ from expected or historic results. You should

understand that it is not possible to predict or identify all such factors.

Consequently, you should not consider any such list to be a complete list of all

potential risks or uncertainties.

Risk

Factors

Investing

in our common stock involves a high degree of risk. Prospective investors should

carefully consider the risks described below, together with all of the other

information included or referred to in this Current Report on Form 8-K, before

purchasing shares of our common stock. There are numerous and varied risks,

known and unknown, that may prevent us from achieving our goals. The risks

described below are not the only risks we will face. If any of these risks

actually occurs, our business, financial condition or results of operations may

be materially adversely affected. In such case, the trading price of our common

stock could decline and investors in our common stock could lose all or part of

their investment. The risks and uncertainties described below are not exclusive

and are intended to reflect the material risks that are specific to us ,

material risks related to our industry and material risks related to companies

that undertake a public offering or seek to maintain a class of securities that

is registered or traded on any exchange or over-the-counter market.

Risks Related to our

Business

We

expect that we will need to raise additional capital in the future; additional

funds may not be available on terms that are acceptable to us, or at

all.

We

anticipate we will have to raise additional capital in the future to service our

debt and to finance our future working capital needs. We cannot assure you that

any additional capital will be available on a timely basis, on acceptable terms,

or at all. Future equity or debt financings may be difficult to obtain. If we

are not able to obtain additional capital as may be required, our business,

financial condition and results of operations could be materially and adversely

affected.

We

anticipate that our capital requirements will depend on many factors,

including:

|

|

·

|

our

ability to repay our existing debt;

|

|

|

·

|

our

ability to fulfill backlog;

|

|

|

·

|

our

ability to procure additional production

contracts;

|

|

|

·

|

our

ability to control costs;

|

|

|

·

|

the

timing of payments and reimbursements from government and other

contracts;

|

|

|

·

|

increased

sales and marketing expenses;

|

|

|

·

|

technological

advancements and competitors’ response to our

products;

|

|

|

·

|

capital

improvements to new and existing

facilities;

|

|

|

·

|

our

relationships with customers and suppliers;

and

|

|

|

·

|

general

economic conditions including the effects of future economic slowdowns,

acts of war or terrorism and the current international

conflicts.

|

Even if

available, financings can involve significant costs and expenses, such as legal

and accounting fees, diversion of management’s time and efforts, and substantial

transaction costs. If adequate funds are not available on acceptable terms, or

at all, we may be unable to finance our operations, develop or enhance our

products, expand our sales and marketing programs, take advantage of future

opportunities or respond to competitive pressures.

Certain

of our products are dependent on specialized sources of supply that are

potentially subject to disruption and attendant adverse impact to our

business.

Some of

our products currently incorporate components purchased from single sources of

supply. If supply from single supply sources is materially disrupted, requiring

us to obtain and qualify alternate sources of supply for such components, our

revenues could decline, our reputation with our customers could be harmed, and

our business and results of operations could be adversely affected.

Current

economic conditions may adversely affect our ability to continue

operations.

Current

economic conditions may cause a decline in business and consumer spending and

capital market performance, which could adversely affect our business and

financial performance. Our ability to raise funds, upon which we are

fully dependent to continue operations, may be adversely affected by current and

future economic conditions, such as a reduction in the availability of credit,

financial market volatility and recession.

Our

historical operations depend on government contracts and

subcontracts. We face additional risks related to contracting with

the federal government, including federal budget issues and fixed price

contracts.

General

political and economic conditions, which cannot be accurately predicted, may

directly and indirectly affect the quantity and allocation of expenditures by

federal agencies. Even the timing of incremental funding commitments to

existing, but partially funded, contracts can be affected by these factors.

Therefore, cutbacks or re-allocations in the federal budget could have a

material adverse impact on our results of our future operations. Obtaining

government contracts may also involve long purchase and payment cycles,

competitive bidding, qualification requirements, delays or changes in funding,

budgetary constraints, political agendas, extensive specification development,

price negotiations and milestone requirements. In addition, our government

contracts are primarily fixed price contracts, which may prevent us from

recovering costs incurred in excess of its budgeted costs. Fixed price contracts

require us to estimate the total project cost based on preliminary projections

of the project’s requirements. The financial viability of any given project

depends in large part on our ability to estimate such costs accurately and

complete the project on a timely basis. Our exposure to the risks of cost

overruns exists in our products business due to the fact that our contracts are

solely of a fixed-price nature. Some of those contracts are for products that

are new to our business and are thus subject to more potential for unanticipated

impacts to manufacturing costs. Given the current economic conditions, it is

also possible that even if our estimates are reasonable at the time made, that

prices of materials are subject to unanticipated adverse

fluctuation. In the event our actual costs exceed the fixed

contractual cost of our product contracts, we will not be able to recover the

excess costs.

Some of

our government contracts are also subject to termination or renegotiation at the

convenience of the government, which could result in a large decline in revenue

in any given quarter. Although government contracts have provisions providing

for the reimbursement of costs associated with termination, the termination of a

material contract at a time when our funded backlog does not permit redeployment

of our staff could result in reductions of employees. Optex generally utilizes

contract and temporary labor to supplement the regular

workforce. This allows the company to mitigate impacts of significant

fluctuations in volume through flexibility in increasing or decreasing the

temporary labor workforce as customer requirements dictate. In

addition, the timing of payments from government contracts is also subject to

significant fluctuation and potential delay, where first article acceptance and

test requirements are required or where a progress billing clause is not

provided for in the contract.. Any such delay could result in a temporary

shortage in our working capital.

If

we fail to scale our operations appropriately in response to growth and changes

in demand, we may be unable to meet competitive challenges or exploit potential

market opportunities, and our business could be materially and adversely

affected.

Our past

growth has placed, and any future growth in our historical business is expected

to continue to place, a significant strain on our management personnel,

infrastructure and resources. To implement our current business and product

plans, we will need to continue to expand, train, manage and motivate our

workforce, and expand our operational and financial systems, as well as our

manufacturing and service capabilities. All of these endeavors will require

substantial management effort and additional capital. If we are unable to

effectively manage our expanding operations, we may be unable to scale our

business quickly enough to meet competitive challenges or exploit potential

market opportunities, and our current or future business could be materially and

adversely affected.

We

do not have long-term employment agreements with our key personnel, other than

our Chief Operating Officer. If we are not able to retain our key personnel or

attract additional key personnel as required, we may not be able to implement

our business plan and our results of operations could be materially and

adversely affected.

We depend

to a large extent on the abilities and continued participation of our executive

officers and other key employees. The loss of any key employee could have a

material adverse effect on our business. We do not presently maintain “key man”

insurance on any key employees. We believe that, as our activities increase and

change in character, additional, experienced personnel will be required to

implement our business plan. Competition for such personnel is intense and we

cannot assure you that they will be available when required, or that we will

have the ability to attract and retain them. In addition, we do not presently

have depth of staffing in our executive, operational and financial management.

Until additional key personnel can be successfully integrated with its

operations, the timing or success of which we cannot currently predict, our

results of operations and ultimate success will be vulnerable to difficulties in

recruiting a new executive management team and losses of key

personnel.

Risks

Relating to the Reorganization

The Company’s directors and executive

officers beneficially own a substantial percentage of the Company’s outstanding

common stock, which gives them control over certain major decisions on which the

Company’s stockholders may vote, which may discourage an acquisition of the

Company.

As a

result of the Reorganization, Sileas Corp. which is owned by one of the

Company’s directors, and two of the Company’s officers, beneficially owns, in

the aggregate, approximately 73% of the Company’s outstanding common stock. The

interests of the Company’s management may differ from the interests of other

stockholders. As a result, the Company’s executive management will have the

right and ability to control virtually all corporate actions requiring

stockholder approval, irrespective of how the Company’s other stockholders may

vote, including the following actions:

|

|

·

|

electing

or defeating the election of

directors;

|

|

|

·

|

amending

or preventing amendment of the Company’s certificate of incorporation or

bylaws;

|

|

|

·

|

effecting

or preventing a merger, sale of assets or other corporate transaction; and

controlling the outcome of any other matter submitted to the stockholders

for vote.

|

The

Company’s management’s beneficial stock ownership may discourage a potential

acquirer from seeking to acquire shares of the Company’s common stock or

otherwise attempting to obtain control of the Company, which in turn could