SCHEDULE

14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

Proxy Statement Pursuant to Section 14(a)

of the

Securities Exchange Act of 1934

Filed by the

registrant ![]()

Filed by a party other than the registrant

![]()

| Check the appropriate box: | ||||||||||||||

| Preliminary proxy statement | Confidential,

for use of the Commission only (as permitted by Rule 14a-6(e)(2)) |

|||||||||||||

| Definitive proxy statement | ||||||||||||||

| Definitive additional materials | ||||||||||||||

| Soliciting material pursuant to Rule 14a-11(c) or Rule 14a-12 | ||||||||||||||

LADENBURG THALMANN FINANCIAL SERVICES INC.

(Name of Registrant as Specified in Its Charter)

(Name of Person(s) Filing Proxy Statement, if Other Than the Registrant)

Payment of filing fee (Check the appropriate box):

| No fee required. |

| Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11. |

| (1) | Title of each class of securities to which transaction applies: |

| (2) | Aggregate amount of securities to which transaction applies: |

| (3) | Per unit price or other underlying value of transaction computed pursuant to Exchange Act Rule 0-11:1 |

| (4) | Proposed maximum aggregate value of transaction: |

| (5) | Total fee paid: |

| Fee paid previously with preliminary materials: ________________________________________ |

| Check box if any part of the fee is offset as provided by Exchange Act Rule 0-11a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous filing by registration statement number, or the form or schedule and the date of its filing. |

| (1) | Amount previously paid: |

| (2) | Form, Schedule or Registration Statement No.: |

| (3) | Filing party: |

| (4) | Date filed: |

| 1 | Set forth the amount on which the filing fee is calculated and state how it was determined. |

LADENBURG

THALMANN FINANCIAL SERVICES INC.

590 Madison Avenue,

34th Floor

New York, New York 10022

NOTICE OF ANNUAL

MEETING

OF SHAREHOLDERS

TO BE HELD ON

, 2004

NOTICE IS HEREBY GIVEN that an annual meeting of shareholders of Ladenburg Thalmann Financial Services Inc., a Florida corporation, will be held at the offices of Ladenburg Thalmann & Co. Inc., our principal operating subsidiary, located at 590 Madison Avenue, 34th Floor, New York, New York, on , , 2004, at 10:00 a.m., for the following purposes, all as more fully described in the attached proxy statement:

| 1. | To elect nine directors to our board of directors to hold office until the next annual meeting of shareholders and until their successors are elected and qualified; |

| 2. | To approve a proposal to issue a total of shares of our common stock to New Valley Corporation and Frost-Nevada Investments Trust, through the conversion of our outstanding senior convertible promissory notes held by such parties, at a price of $1.10 per share for New Valley and $0.70 per share for Frost-Nevada; and |

| 3. | To transact such other business as may properly come before the meeting, and any or all postponements or adjournments thereof. |

Only shareholders of record at the close of business on , 2004, will be entitled to notice of, and to vote at, the meeting and any postponements or adjournments.

You are urged to read the attached proxy statement, which contains information relevant to the actions to be taken at the meeting. Whether or not you expect to attend the meeting in person, please sign and date the accompanying proxy card and mail it promptly in the enclosed addressed, postage-prepaid envelope. You may revoke your proxy if you so desire at any time before it is voted.

| By Order of the Board of Directors |

| Charles I. Johnston, President and Chief Executive Officer |

New York, New York

,

2004

LADENBURG THALMANN FINANCIAL SERVICES INC.

PROXY STATEMENT

ANNUAL MEETING OF

SHAREHOLDERS

TO BE HELD ON

, 2004

This proxy statement and the enclosed form of proxy are furnished in connection with solicitation of proxies by our board directors for use at an annual meeting of shareholders to be held on , 2004, and any postponements or adjournments.

On or about , 2004, this proxy statement and the accompanying form of proxy are being mailed to each shareholder of record at the close of business on , 2004.

The information provided in the "question and answer" format below is for your convenience only and is merely a summary of the information contained in this proxy statement. You should read this proxy statement carefully.

What matters am I voting on?

You will be voting on:

| • | the election of nine directors to hold office until the next annual meeting of shareholders and until their successors are elected and qualified; |

| • | the approval of a proposal to issue shares of our common stock to New Valley Corporation and Frost-Nevada Investments Trust, through the conversion of our outstanding senior convertible promissory notes held by such parties (the "Debt Conversion"), at a price of $1.10 per share for New Valley and $0.70 per share for Frost-Nevada; and |

| • | any other business that may properly come before the meeting. |

Who is entitled to vote?

Holders of our common stock as of the close of business on , 2004, the record date, are entitled to vote at the meeting. As of the record date, we had issued and outstanding 44,191,416 shares of common stock, our only class of voting securities outstanding. Each holder of our common stock is entitled to one vote for each share held on the record date.

What is the effect of giving a proxy?

Proxies in the form enclosed are solicited by and on behalf of our board. The persons named in the proxy have been designated as proxies by our board. If you sign and return the proxy in accordance with the procedures set forth in this proxy statement, the persons designated as proxies by the board will vote your shares at the meeting as specified in your proxy.

If you sign and return your proxy in accordance with the procedures set forth in this proxy statement but you do not provide any instructions as to how your shares should be voted, your shares will be voted FOR the election as directors of the nominees listed below under Proposal 1 and FOR the approval of the proposal to issue shares of our common stock to New Valley and Frost-Nevada upon conversion of their outstanding senior convertible promissory notes as described below under Proposal 2. If you give your proxy, your shares will also be voted in the discretion of the proxies named on the proxy card with respect to any other matters properly brought before the meeting.

1

Can I change my vote after I return my proxy card?

You may revoke your proxy at any time before it is exercised by:

| • | delivering written notification of your revocation to our secretary; |

| • | voting in person at the meeting; or |

| • | delivering another proxy bearing a later date. |

Please note that your attendance at the meeting will not alone serve to revoke your proxy.

What is a quorum?

A quorum is the minimum number for shares required to be present at the meeting for the meeting to be properly held under our bylaws and Florida law. The presence, in person or by proxy, of a majority of all outstanding shares of common stock entitled to vote at the meeting will constitute a quorum at the meeting. A proxy submitted by a shareholder may indicate that all or a portion of the shares represented by the proxy are not being voted ("shareholder withholding") with respect to a particular matter. Similarly, a broker may not be permitted to vote stock ("broker non-vote") held in street name on a particular matter in the absence of instructions from the beneficial owner of the stock. The shares subject to a proxy which are not being voted on a particular matter because of either shareholder withholding or broker non-vote will not be considered shares present and entitled to vote on that matter. These shares, however, may be considered present and entitled to vote on other matters and will count for purposes of determining the presence of a quorum if the shares are being voted with respect to any matter at the meeting. If the proxy indicates that the shares are not being voted on any matter at the meeting, the shares will not be counted for purposes of determining the presence of a quorum. Abstentions are voted neither "for" nor "against" a matter but are counted in the determination of a quorum.

How may I vote?

You may vote your shares by mail. Date, sign and return the accompanying proxy in the envelope enclosed for that purpose (to which no postage need be affixed if mailed in the United States). You may specify your choices by marking the appropriate boxes on the proxy card. If you attend the meeting, you may deliver your completed proxy card in person or fill out and return a ballot that will be supplied to you.

How many votes are needed for approval of each matter?

The election of directors requires a plurality vote of the shares of common stock voted at the meeting. "Plurality" means that the individuals who receive the largest number of votes cast "FOR" are elected as directors. Consequently, any shares not voted "FOR" a particular nominee (whether as a result of a direction of the securities holder to withhold authority, abstentions or a broker non-vote) will not be counted in such nominee's favor. As there are nine directors to be elected, the nine persons receiving the highest votes will be elected if nominees other than those nominated by the board are presented.

The proposal to issue shares of our common stock to New Valley and Frost-Nevada upon conversion of their outstanding senior convertible promissory notes as described below under Proposal 2 must be approved by a majority of the votes cast at the meeting with respect to the proposal. Abstentions and shares deemed present at the meeting but not entitled to vote with respect to each of the proposals (because of either shareholder withholding or broker non-vote) are not deemed voted and therefore will have no effect on such vote. Pursuant to the Debt Conversion Agreement described below under Proposal 2, certain current and former members of our board of directors have agreed to vote the shares of our common stock held by them on the date of the agreement in accordance with the vote of a majority of votes cast at the meeting, excluding the shares held by such parties.

Any other proposal properly brought at the annual meeting must be approved by a majority of the votes cast at the meeting with respect to the proposal.

2

Annual Report

We will provide, without charge, a copy of our Annual Report on Form 10-K for the fiscal year ended December 31, 2003, which includes our audited financial statements, upon the written request of any person stating that (s)he is a beneficial holder of our common stock. Requests for copies and inquiries should be sent in writing to Investor Relations Department, Ladenburg Thalmann Financial Services Inc., 590 Madison Avenue, 34th Floor, New York, New York 10022.

Security Ownership of Certain Beneficial Owners and Management

The following table sets forth certain information as of , 2004 with respect to the beneficial ownership of our common stock before and after giving effect to the Debt Conversion, assuming no issuances or conversions of other outstanding convertible securities prior to the Debt Conversion, by (i) those persons or groups known to beneficially own more than 5% of our voting securities, (ii) each of our directors, (iii) each of the executive officers named in the Summary Compensation Table below and (iv) all of our current directors and executive officers as a group. Except as otherwise stated, the business address of each of the below listed persons is c/o Ladenburg Thalmann Financial Services Inc., 590 Madison Avenue, 34th Floor, New York, New York 10022.

| Beneficial

ownership(1) of our common stock prior to the Debt Conversion |

Beneficial ownership of our common stock following the Debt Conversion(2) |

|||||||||||||||||

| Name of Beneficial Owner | Number of Shares |

Percent | Number of Shares |

Percent | ||||||||||||||

| Phillip Frost, M.D. (3) | (4) | % | (5) | % | ||||||||||||||

| Berliner Effektengesellschaft AG(6) | 4,620,501 | 10.6 | % | 4,620,501 | % | |||||||||||||

| Bennett S. LeBow | 4,381,314 | (7) | 10.0 | % | 4,381,314 | (7) | % | |||||||||||

| Richard J. Rosenstock | 3,968,012 | (8) | 9.0 | % | 3,968,012 | (8) | % | |||||||||||

| New Valley Corporation(9) | (10) | % | (11) | % | ||||||||||||||

| Carl C. Icahn(12) | 3,396,258 | (13) | 7.8 | % | 3,396,258 | (12) | % | |||||||||||

| Mark Zeitchick | 1,692,977 | (13) | 3.9 | % | 1,692,977 | (14) | % | |||||||||||

| Vincent Mangone | 1,692,977 | (15) | 3.9 | % | 1,692,977 | (15) | % | |||||||||||

| Howard M. Lorber | 1,555,878 | (16) | 3.6 | % | 1,555,878 | (16) | % | |||||||||||

| Victor M. Rivas | 879,466 | (17) | 2.0 | % | 879,466 | (17) | % | |||||||||||

| Richard J. Lampen | 78,367 | (18) | * | 78,367 | (18) | * | ||||||||||||

| Robert J. Eide | 51,367 | (19) | * | 51,367 | (19) | * | ||||||||||||

| Henry C. Beinstein | 51,361 | (20) | * | 51,361 | (20) | * | ||||||||||||

| Salvatore Giardina | 23,333 | (21) | * | 23,333 | (21) | * | ||||||||||||

| Charles I. Johnston | 0 | (22) | 0 | 0 | (22) | 0 | ||||||||||||

| All directors and executive officers as a group (10 persons) | (23) | % | (24) | % | ||||||||||||||

| * | Less than 1 percent. |

| (1) | Beneficial ownership is determined in accordance with Rule 13d-3 under the Securities Exchange Act of 1934. The information concerning the shareholders is based upon numbers reported by the owner in documents publicly filed with the SEC, publicly available information or information made known to us. Except as otherwise indicated, all of the shares of common stock are owned of record and beneficially and the persons identified have sole voting and investment power with respect thereto. |

| (2) | Assumes the issuance of shares of common stock upon conversion of the principal and accrued but unpaid interest on the senior convertible promissory notes held by New Valley and Frost-Nevada to take place promptly following the annual meeting. If the annual meeting is |

3

| adjourned for any reason, the number of shares to be issued will be increased to an amount obtained by dividing the principal and accrued but unpaid interest on the date the meeting is ultimately held by the respective conversion prices for each of New Valley and Frost-Nevada. |

| (3) | The business address of Dr. Frost is c/o IVAX Corporation, 4400 Biscayne Boulevard, Miami, Florida 33137. |

| (4) | Represents (i) 1,844,366 shares of common stock held by Frost Gamma Investments Trust, a trust organized under Florida law, (ii) 100,000 shares of common stock issuable upon exercise of an immediately exercisable warrant held by Frost Gamma, (iii) shares of common stock issuable as of the record date upon conversion of the principal and accrued but unpaid interest on a senior convertible promissory note held by Frost-Nevada Investments Trust, a trust organized under Florida law, and (iv) 20,000 shares of common stock issuable upon exercise of currently exercisable options held by Dr. Frost. Dr. Frost is the sole trustee of both Frost Gamma Investments Trust and Frost-Nevada Investments Trust. As the sole trustee of the Gamma Trust and the Nevada Trust, Dr. Frost may be deemed the beneficial owner of all shares owned by the Gamma Trust and the Nevada Trust, respectively, by virtue of his power to vote or direct the vote of such shares or to dispose or direct the disposition of such shares owned by such trusts. Accordingly, solely for purposes of reporting beneficial ownership of such shares pursuant to Section 13(d) of the Securities Exchange Act of 1934, as amended, each of these persons will be deemed to be the beneficial owner of the shares held by any other such person. The foregoing information was derived from an Amendment to Schedule 13D filed with the SEC on April 12, 2004 as well as from information made known to us. |

| (5) | Represents the same shares referred to in footnote 4 above except that the shares of common stock issuable upon conversion of the principal and accrued but unpaid interest on the senior convertible promissory note held by Frost-Nevada have been replaced with shares of common stock held by Frost-Nevada as a result of the Debt Conversion. |

| (6) | The business address for Berliner Effektengesellschaft AG is Kurfüstendamm 119, 10711 Berlin, Germany. |

| (7) | Represents (i) 758,205 shares of common stock held directly by Mr. LeBow, (ii) 3,325,199 shares of common stock held by LeBow Gamma Limited Partnership, a Nevada limited partnership, (iii) 110,336 shares of common stock held by LeBow Alpha LLLP, a Delaware limited liability limited partnership, (iv) 147,574 shares of common stock held by The Bennett and Geraldine LeBow Foundation, Inc., a Florida not-for-profit corporation, and (v) 40,000 shares of common stock issuable upon exercise of currently exercisable options held by Mr. LeBow. Does not include the shares of common stock beneficially owned by New Valley Corporation of which Mr. LeBow serves as an executive officer and director. Mr. LeBow indirectly exercises sole voting power and sole dispositive power over the shares of common stock held by the partnerships. LeBow Holdings, Inc., a Nevada corporation, is the sole stockholder of LeBow Gamma, Inc., a Nevada corporation, which is the general partner of LeBow Gamma Limited Partnership, and is the general partner of LeBow Alpha LLLP. Mr. LeBow is a director, officer and sole stockholder of LeBow Holdings, Inc. and a director and officer of LeBow Gamma, Inc. Mr. LeBow and family members serve as directors and executive officers of the Foundation and Mr. LeBow possesses shared voting and shared dispositive power with the other directors of the Foundation with respect to the Foundation's shares of common stock. The foregoing information was derived from an Amendment to Schedule 13D filed with the SEC on April 2, 2004 as well as from information made known to us. |

| (8) | Represents (i) 3,701,346 shares of common stock held of record by The Richard J. Rosenstock Revocable Living Trust Dated 3/5/96, of which Mr. Rosenstock is the sole trustee and beneficiary, and (ii) 266,666 shares of common stock issuable upon exercise of currently exercisable options held by Mr. Rosenstock. Does not include 83,334 shares of common stock issuable upon exercise of options held by Mr. Rosenstock that are not currently exercisable and that will not become exercisable within the next 60 days. |

4

| (9) | The business address for New Valley Corporation is 100 S. E. Second Street, Miami, Florida 33131. |

| (10) | Represents (i) shares of common stock issuable as of the record date upon conversion of principal and accrued but unpaid interest on a senior convertible promissory note held by New Valley and (ii) 100,000 shares of common stock issuable upon exercise of immediately exercisable warrants held by New Valley. The foregoing information was derived from an Amendment to Schedule 13D filed with the SEC on April 2, 2004 as well as from information made known to us. |

| (11) | Represents shares of common stock and 100,000 shares of common stock issuable upon exercise of immediately exercisable warrants held by New Valley. |

| (12) | The business address for Mr. Icahn is c/o Icahn Associates Corp., 767 Fifth Avenue, 47th Floor, New York, New York 10153. |

| (13) | Represents (i) 2,148,725 shares of common stock held by High River Limited Partnership, (ii) 1,227,773 shares of common stock held by Tortoise Corp. and (iii) 19,760 shares of common stock held by Little Meadow Corp. Each of these entities are either directly or indirectly 100% owned by Mr. Icahn. As such, Mr. Icahn is in a position to directly and indirectly determine the investment and voting decisions made by these entities. Accordingly, Mr. Icahn may be deemed to be the beneficial owner of these shares for purposes of reporting beneficial ownership pursuant to Section 13(d) of the Exchange Act. However, Mr. Icahn disclaims beneficial ownership of these shares for all other purposes. The foregoing information was derived from a Schedule 13D filed with the SEC on December 28, 2001. |

| (14) | Represents (i) 1,426,311 shares of common stock held of record by MZ Trading LLC, of which Mr. Zeitchick is the sole managing member, (ii) 100,000 shares of common stock issuable upon exercise of currently exercisable options held by Mr. Zeitchick and (iii) 166,666 shares of common stock issuable upon exercise of currently exercisable options held by MZ Trading. Does not include 83,334 shares of common stock issuable upon exercise of options held by MZ Trading that are not currently exercisable and that will not become exercisable within the next 60 days. |

| (15) | Represents (i) 1,426,311 shares of common stock held of record by The Vincent A. Mangone Revocable Living Trust Dated 11/5/96, of which Mr. Mangone is the sole trustee and beneficiary, and (ii) 266,666 shares of common stock issuable upon exercise of currently exercisable options held by Mr. Mangone. Does not include 83,334 shares of common stock issuable upon exercise of options held by Mr. Mangone that are not currently exercisable and that will not become exercisable within the next 60 days. |

| (16) | Represents (i) 1,392,251 shares of common stock held directly by Mr. Lorber, (ii) 118,560 shares of common stock held by Lorber Alpha II Partnership, a Nevada limited partnership, (iii) 5,067 shares of common stock held by the Lorber Charitable Fund, a New York not-for-profit corporation, and (iv) 40,000 shares of common stock issuable upon exercise of currently exercisable options held by Mr. Lorber. Does not include (i) 20,000 shares of common stock issuable upon exercise of options held by Mr. Lorber that are not currently exercisable and that will not become exercisable within 60 days and (ii) the shares of common stock beneficially owned by New Valley Corporation of which Mr. Lorber serves as an executive officer and director. Mr. Lorber indirectly exercises sole voting power and sole dispositive power over the shares of common stock held by the partnership. Lorber Alpha II, Inc., a Nevada corporation, is the general partner of Lorber Alpha II Partnership. Mr. Lorber is the director, officer and principal stockholder of Lorber Alpha II, Inc. Mr. Lorber and family members serve as directors and executive officers of Lorber Charitable Fund, and Mr. Lorber possesses shared voting power and shared dispositive power with the other directors of the fund with respect to the fund's |

5

| shares of our common stock. The foregoing information was derived from an Amendment to Schedule 13D filed with the SEC on December 21, 2001 as well as from information made known to us. |

| (17) | Includes 866,666 shares of common stock issuable upon exercise of currently exercisable options held by Mr. Rivas. |

| (18) | Includes 40,000 shares of common stock issuable upon exercise of currently exercisable options held by Mr. Lampen. Does not include (i) 20,000 shares of common stock issuable upon exercise of options held by Mr. Lampen that are not currently exercisable and that will not become exercisable within the next 60 days and (ii) the shares of common stock beneficially owned by New Valley Corporation of which Mr. Lampen serves as an executive officer and director. |

| (19) | Includes 40,000 shares of common stock issuable upon exercise of currently exercisable options held by Mr. Eide. Does not include 20,000 shares of common stock issuable upon exercise of options held by Mr. Eide that are not currently exercisable and that will not become exercisable within 60 days. |

| (20) | Includes (i) 823 shares of common stock held of record in the individual retirement account of Mr. Beinstein's spouse and (ii) 40,000 shares of common stock issuable upon exercise of currently exercisable options held by Mr. Beinstein. Does not include 20,000 shares of common stock issuable upon exercise of options held by Mr. Beinstein that are not currently exercisable and that will not become exercisable within 60 days. |

| (21) | Includes 23,333 shares of common stock issuable upon exercise of currently exercisable options held by Mr. Giardina. Does not include 41,667 shares of common stock issuable upon exercise of options held by Mr. Giardina that are not currently exercisable and that will not become exercisable within the next 60 days. |

| (22) | Does not include 2,500,000 shares of common stock issuable upon exercise of options held by Mr. Johnston that are not currently exercisable and that will not become exercisable within the next 60 days. |

| (23) | Includes shares of common stock issuable upon exercise of currently exercisable options and conversion of principal and accrued but unpaid interest on senior convertible promissory notes. See notes 3, 7, 15, 17, 18, 19 and 20. Excludes 2,705,001 shares of common stock issuable upon exercise of options that are not currently exercisable and that will not become exercisable within the next 60 days. See notes 7, 15, 17, 18, 19, 20 and 21. |

| (24) | Includes 569,999 shares of common stock issuable upon exercise of currently exercisable options and conversion of senior convertible promissory notes. See notes 4, 7, 15, 17, 18, 19 and 20.Excludes 2,705,001 shares of common stock issuable upon exercise of options that are not currently exercisable and that will not become exercisable within the next 60 days. See notes 7, 15, 17, 18, 19, 20 and 21. |

6

PROPOSAL I

ELECTION OF DIRECTORS

At this year's annual meeting of shareholders, nine directors will be elected to hold office for a term of one year expiring at the next annual meeting of shareholders. Each director will be elected to serve until a successor is elected and qualified or until the director's earlier resignation or removal.

Unless authority is withheld, the proxies solicited by the board of directors will be voted FOR the election of these nominees. Our articles of incorporation do not provide for cumulative voting. In case any of the nominees becomes unavailable for election to the board of directors, an event which is not anticipated, the persons named as proxies, or their substitutes, will have full discretion and authority to vote or refrain from voting for any other candidate in accordance with their judgment. The nine nominees for directors, their current positions with us, their term of office and their business background are set forth below.

Howard M. Lorber, 55 years old, has been chairman of our board of directors since May 2001. Since November 1994, he has been president, chief operating officer and a member of the board of directors of New Valley, a company engaged in the real estate business and seeking to acquire additional operating companies. From January 1994 to January 2001, Mr. Lorber was a consultant to Vector Group Ltd., a New York Stock Exchange-listed holding company, with subsidiaries engaged in the manufacture and sale of cigarettes and the principal shareholder of New Valley, and since January 2001 has served as its president, chief operating officer and a member of its board of directors. Mr. Lorber has been chairman of the board of directors of Hallman & Lorber Associates Inc., consultants and actuaries of qualified pension and profit sharing plans, and various of its affiliates since 1975. Mr. Lorber has been a stockholder and a registered representative of Aegis Capital Corp., a broker-dealer and a member firm of the NASD since 1984. Since 1990, Mr. Lorber has been chairman of the board of directors of Nathan's Famous, Inc., a chain of fast food restaurants, and has been its chief executive officer since 1993. Mr. Lorber also serves as a director of United Capital Corp., a real estate investment and diversified manufacturing company, and of Prime Hospitality Corp., a company doing business in the lodging industry. He is also a trustee of Long Island University.

Charles I. Johnston, 50 years old, has been our president, chief executive officer and a member of our board of directors since April 2004. He has also been the chairman and chief executive officer of Ladenburg Thalmann & Co. Inc., our operating subsidiary, since April 2004. From June 1996 until March 2004, Mr. Johnston served in various capacities with Lehman Brothers Inc., including most recently as a managing director and the global head of private client services.

Phillip Frost, M.D., 67 years old, has been a member of our board of directors since March 2004. He also served as a member of our board of directors from May 2001 until July 2002. Dr. Frost has served as chairman of the board of directors and chief executive officer of IVAX Corporation, an American Stock Exchange-listed company engaged in the research, development, manufacture and marketing of pharmaceutical products, since 1987. From July 1991 until January 1995, he also served as the president of IVAX. He has also served as chairman of the board of directors of IVAX Diagnostics, Inc., an American Stock Exchange-listed company that produces diagnostic reagent kits and is a subsidiary of IVAX, since March 2001. Dr. Frost was the chairman of the Department of Dermatology at Mt. Sinai Medical Center of Greater Miami, Miami Beach, Florida from 1972 to 1990. Dr. Frost was chairman of the board of directors of Key Pharmaceuticals, Inc. from 1972 to 1986. He is a director of Continucare Corporation, an American Stock Exchange-listed provider of outpatient healthcare and home healthcare services, and Northrop Grumman Corp., an aerospace company. He is chairman of the board of trustees of the University of Miami and a member of the board of governors of the American Stock Exchange.

Henry C. Beinstein, 61 years old, has been a member of our board of directors since May 2001. Mr. Beinstein has been a director of New Valley since 1994 and of Vector Group since March 2004. Since August 2002, Mr. Beinstein has been a money manager and an analyst and registered representative of Gagnon Securities, LLC, a broker-dealer and a member firm of the NASD. He retired in August 2002 as the executive director of Schulte Roth & Zabel LLP, a New York-based law

7

firm, a position he had held since August 1997. Before that, Mr. Beinstein had served as the managing director of Milbank, Tweed, Hadley & McCloy LLP, a New York-based law firm, commencing in November 1995. From April 1985 through October 1995, Mr. Beinstein was the executive director of Proskauer Rose LLP, a New York-based law firm. Mr. Beinstein is a certified public accountant in New York and New Jersey and prior to joining Proskauer was a partner and national director of finance and administration at Coopers & Lybrand.

Robert J. Eide, 51 years old, has been a member of our board of directors since May 2001. He has also been the chairman and chief executive officer of Aegis Capital Corp. since before 1988. Mr. Eide also serves as a director of Nathan's Famous and Vector Group.

Richard J. Lampen, 50 years old, has been a member of our board of directors since January 2002. He has been the executive vice president and general counsel of New Valley since October 1995 and a member of its board of directors since July 1996. Since July 1996, Mr. Lampen has served as executive vice president of Vector Group. Since January 1997, Mr. Lampen has served as a director of CDSI Holdings Inc., a company with interests in the marketing services business, and since November 1998 has been its president and chief executive officer. From May 1992 to September 1995, Mr. Lampen was a partner at Steel Hector & Davis, a law firm located in Miami, Florida. From January 1991 to April 1992, Mr. Lampen was a managing director at Salomon Brothers Inc., an investment bank, and was an employee at Salomon Brothers from 1986 to April 1992. Mr. Lampen has served as a director of a number of other companies, including U.S. Can Corporation, The International Bank of Miami, N.A. and Spec's Music Inc., as well as a court-appointed independent director of Trump Plaza Funding, Inc.

Richard J. Rosenstock, 52 years old, has been a member of our board of directors since August 1999. From May 2001 until December 2002, Mr. Rosenstock served as vice chairman of our board of directors and from August 1999 until December 2002, served as our chief operating officer. He also served as our president from August 1999 until May 2001. Since January 2003, Mr. Rosenstock has been a registered representative of Ladenburg. Mr. Rosenstock was affiliated with Ladenburg Capital Management Inc., one of our former operating subsidiaries, from 1986 until December 2002, serving from May 2001 as Ladenburg Capital Management's chief executive officer. From January 1994 until May 1998, he served as an executive vice president of Ladenburg Capital Management and was its president from May 1998 until November 2001.

[Additional Directors]

Independence of Directors

Our common stock is listed on the American Stock Exchange. As a result, we follow the rules of the Exchange in determining if a director is independent. The board of directors also consults with our counsel to ensure that the board of directors' determinations are consistent with those rules and all relevant securities and other laws and regulations regarding the independence of directors. Consistent with these considerations, the board of directors affirmatively has determined that Messrs. Frost, Beinstein, Eide, and will be our independent directors for the upcoming year. The other remaining directors would not be deemed independent under the Exchange's rules because they are currently employed by us or have other prior or existing relationships with us that results in them being deemed not "independent."

Code of Ethics

In February 2004, our board of directors adopted a code of ethics that applies to our directors, officers and employees as well as those of our subsidiaries. A copy of our code of ethics has been filed as an exhibit to our Annual Report on Form 10-K for the year ended December 31, 2003. Requests for copies of our code of ethics should be sent in writing to Investor Relations Department, Ladenburg Thalmann Financial Services Inc., 590 Madison Avenue, 34th Floor, New York, New York 10022.

Board and Committee Information

During the fiscal year ended December 31, 2003, our board of directors met one time and acted by unanimous written consent two times. In 2003, two members of our board of directors attended our

8

annual meeting. Although we do not have any formal policy regarding director attendance at annual shareholder meetings, we attempt to schedule our annual meetings so that all of our directors can attend. In addition, we expect our directors to attend all board and committee meetings and to spend the time needed and meet as frequently as necessary to properly discharge their responsibilities. We have standing nominating, compensation and audit committees of the board of directors. Each of our current directors attended at least 75% of the aggregate number of meetings of the board and of each committee of which he was a member held in 2003.

Nominating Committee Information

Our nominating committee was formed in February 2004 and consists of Henry C. Beinstein and Robert J. Eide, each of whom are independent directors. The nominating committee is responsible for overseeing the selection of persons to be nominated as our directors. The nominating committee considers persons identified by its members, management, investors, investment bankers and others. The nominating committee does not have a written charter, nor does it have any formal criteria for nominees. However, we feel that persons to be nominated should be actively engaged in business endeavors, have an understanding of financial statements, corporate budgeting and capital structure, and be willing to devote significant time to the promotion of the oversight duties of the board of directors of a public company. For more information regarding our nomination process, see the section entitled "2005 Annual Meeting Shareholder Proposals and Nominations" below.

At the annual meeting to which this proxy relates, some of the persons to be elected are current executive officers and directors standing for re-election. Additionally, some of the persons to be elected were recommended by our non-management directors currently standing for re-election.

As the nominating committee was not formed until February 2004, it did not meet during the fiscal year ended December 31, 2003.

Compensation Committee Information and Report

The compensation committee was established in November 1999 and is currently comprised of Henry C. Beinstein, Robert J. Eide and Howard M. Lorber. Following the annual meeting, Mr. Lorber will be replaced with to serve on the compensation committee. The compensation committee is responsible for administering our Annual Incentive Bonus Plan ("Bonus Plan"), our Special Performance Incentive Plan ("Incentive Plan") and our 1999 Performance Equity Plan ("Equity Plan"). During the fiscal year ended December 31, 2003, the compensation committee acted by unanimous written consent three times.

Compensation Committee Report on Executive Compensation

This report is made by our compensation committee, which consists of three non-employee directors. The responsibilities of the committee include:

| • | establishing the general compensation policy for our executive officers, including our chief executive officer; |

| • | administering our Bonus Plan, Incentive Plan and Equity Plan, each of which is designed to comply with the requirements of Section 162(m) of the Internal Revenue Code; and |

| • | in administering each of these plans, determining who participates in the plans, establishing performance goals, if any, and determining specific grants and bonuses to the participants. |

The committee's executive compensation policies are generally designed to provide competitive levels of compensation that integrate pay with our annual performance and reward above average corporate performance, recognize individual initiative and achievements, and assist us in attracting and retaining qualified executives. Our agreements with our executive officers have generally included compensation in the form of (i) a base salary, which was not anticipated to be the sole component of our executives total annual cash compensation, (ii) brokerage commissions with respect to customer accounts for which such individuals were the designated account representatives, (iii) participation in

9

our Bonus Plan and Incentive Plan that was designed to provide additional cash compensation based upon our achieving specific criteria and performance targets and (iv) a grant of stock options under our Equity Plan.

Our Bonus Plan is a performance-based compensation plan which provides for the payment of bonuses to participants selected by the committee if performance targets established by the committee are met within the specified performance periods. For the fiscal year ended December 31, 2003, the committee determined at the beginning of the period that participating employees would participate in a bonus pool equal to 25% of our net income before taxes and before the accrual of compensation payable under this plan, provided that we achieved a 10% return on equity before taxes at the end of the fiscal year. For the fiscal year ended December 31, 2003, the predetermined target was not met and no awards were made under this plan.

Our Incentive Plan is similar in nature to our Bonus Plan in that participants selected by the committee at the beginning of the year are permitted to receive bonuses upon reaching performance targets established by the committee within specific performance periods, which performance targets can be based upon one or more selected business criteria. For the fiscal year ended December 31, 2003, the committee determined that the participants would be entitled to receive a bonus that is based upon total consolidated revenues provided that specified commission levels are achieved. These bonuses are paid monthly, based on the average monthly revenues to such date. Final awards reflecting the performance for the last month of the fiscal year and the fiscal year overall are not paid until the financial results for the year are reconciled and the committee has approved and certified that the established performance requirements have been achieved. During the fiscal year ended December 31, 2003, the performance targets were achieved and bonuses were paid to the participants based upon percentages established by the committee when it selected the participants.

Our Equity Plan was adopted by our shareholders in August 1999 under which our officers, directors, key employees and consultants are eligible to receive stock options, stock appreciation rights, restricted stock awards and other stock based awards. We may issue grants to executives upon their employment or at subsequent dates based on recommendations made by our senior management to the committee.

Compensation of the Chief Executive Officer

Victor Rivas served as our president and chief executive officer during the fiscal year ended December 31, 2003. Mr. Rivas' base salary for such year was determined in accordance with the employment agreement that we entered into with him in May 2001. Mr. Rivas' base salary was at the rate of $500,000 per year subject to periodic increases as determined by our board of directors or our compensation committee. As a portion of his compensation for the fiscal year ended December 31, 2003, Mr. Rivas received a guaranteed bonus of $500,000 paid in accordance with the terms of his employment agreement.

The Members of the Compensation Committee

| Henry C. Beinstein Robert J. Eide Howard M. Lorber |

Compensation Committee Interlocks and Insider Participation

Our compensation committee is comprised of Messrs. Beinstein, Eide and Lorber. None of these individuals served as an officer of our company or of our subsidiaries.

Victor M. Rivas, our former president and chief executive officer, serves as a member of New Valley's board of directors, of which Mr. Lorber is president, chief operating officer and a director. Additionally, Richard J. Lampen, New Valley's executive vice president, general counsel and director, is a member of our board of directors. No individual who is an executive officer of ours currently serves on the New Valley compensation committee.

10

Audit Committee Information and Report

Our audit committee was established in November 1999 and is currently comprised of Henry C. Beinstein, Robert J. Eide and Richard J. Lampen, with Mr. Beinstein serving as the chairman of the committee. Following the annual meeting, Mr. Lampen will be replaced with to serve on the audit committee. Except pursuant to limited exceptions, our audit committee is required by the American Stock Exchange to be made up of at least three "independent directors" who are also "financially literate" as defined in the standards. These listing standards define an "independent director" generally as a person, other than an officer of the company, who does not have a relationship with the company that would interfere with the director's exercise of independent judgment. The listing standards define "financially literate" as being able to read and understand fundamental financial statements (including a company's balance sheet, income statement and cash flow statement).

Financial Expert on Audit Committee

Our board of directors believes that the audit committee has at least one "audit committee financial expert" (as defined in Regulation 240.401(h)(1)(i)(A) of Regulation S-K) serving on its audit committee, such "audit committee financial expert" being Mr. Beinstein. Our board of directors also believes that Mr. Beinstein would be considered an "independent" director under Item 7(d)(3)(iv) of Schedule 14A under the Securities Exchange Act of 1934.

Meetings and Attendance

During the fiscal year ended December 31, 2003, the audit committee met four times.

Audit Fees

For the fiscal years ended December 31, 2003 and 2002, the aggregate fees billed for professional services rendered by our principal accountant for the audit of our annual financial statements and review of financial statements included in our quarterly reports on Form 10-Q or services that are normally provided by the accountant in connection with statutory and regulatory filings or engagements for those fiscal years were $186,250 and $165,500, respectively.

Audit-Related Fees

For the fiscal years ended December 31, 2003 and 2002, the aggregate fees billed for assurance and related services by our principal accountant that are reasonably related to the performance of the audit or review of our financial statements and are not reported under the paragraph entitled "Audit Fees" above were $23,000 and $20,000, respectively. These fees were for the audit of our 401(k) retirement plan.

Tax Fees

For the fiscal years ended December 31, 2003 and 2002, the aggregate fees billed for professional services rendered by our principal accountant for tax compliance, tax advice, and tax planning were $37,750 and $59,500, respectively. The services performed include the preparation of our federal, state and local income tax returns for the fiscal years ended September 30, 2003 and 2002, federal net operating loss carryback returns and the tax returns of the Ladenburg Focus Fund, L.P., one of our private investment funds.

All Other Fees

For the fiscal years ended December 31, 2003 and 2002, the aggregate fees billed for products and services provided by our principal accountant, other than the services reported above were $9,000 and $0, respectively. The services performed were agreed upon procedures relating to Ladenburg's compliance with the anti-money laundering requirements of the USA PATRIOT Act of 2001.

11

Audit Committee Pre-Approval Policies and Procedures

In accordance with Section 10A(i) of the Securities Exchange Act of 1934, before we engage our independent accountant to render audit or non-audit services, the engagement is approved by our audit committee. Our audit committee approved all of the fees referred to in the sections entitled "Audit Fees," Audit-Related Fee," "Tax Fees" and "All Other Fees" above.

Audit Committee Report

Pursuant to the audit committee's written charter, which was adopted on June 29, 2000, as amended and restated on August 12, 2003, our audit committee's responsibilities include, among other things:

| • | reviewing and discussing with management and the independent auditor the annual audited financial statements, and recommending to the board whether the audited financial statements should be included in our Form 10-K; |

| • | discussing with management and the independent auditor significant financial reporting issues and judgments made in connection with the preparation of our financial statements; |

| • | discussing with management and the independent auditor the effect on our financial statements of (i) regulatory and accounting initiatives and (ii) off-balance sheet structures; |

| • | discussing with management major financial risk exposures and the steps management has taken to monitor and control such exposures, including our risk assessment and risk management policies; |

| • | reviewing disclosures made to the audit committee by our chief executive officer and chief financial officer during their certification process for our Form 10-K and Form 10-Q about any significant deficiencies in the design or operation of internal controls or material weaknesses therein and any fraud involving management or other employees who have a significant role in our internal controls; |

| • | verifying the rotation of the lead (or coordinating) audit partner having primary responsibility for the audit and the audit partner responsible for reviewing the audit as required by law; |

| • | reviewing and approving all related-party transactions; |

| • | inquiring and discussing with management our compliance with applicable laws and regulations; |

| • | pre-approving all auditing services and permitted non-audit services to be performed by our independent auditor, including the fees and terms of the services to be performed; |

| • | appointing or replacing the independent auditor; |

| • | determining the compensation and oversight of the work of the independent auditor (including resolution of disagreements between management and the independent auditor regarding financial reporting) for the purpose of preparing or issuing an audit report or related work; and |

| • | establishing procedures for the receipt, retention and treatment of complaints received by us regarding accounting, internal accounting controls or reports which raise material issues regarding our financial statements or accounting policies. |

Our audit committee has met and held discussions with management and our independent auditors. Management represented to the committee that our consolidated financial statements were prepared in accordance with generally accepted accounting principles, and the committee has reviewed and discussed the consolidated financial statements with management and the independent auditors. The committee discussed with the independent auditors the matters required to be discussed by Statement on Auditing Standards No. 61 (Communication with Audit Committees). Our independent auditors also provided the audit committee with the written disclosures required by Independence

12

Standards Board Standard No. 1(Independence Discussions with Audit Committees) and the committee discussed with the independent auditors and management the auditors' independence, including with regard to fees for services rendered during the fiscal year and for all other professional services rendered by our independent auditors. Based upon the committee's discussion with management and the independent auditors and the committee's review of the representations of management and the report of the independent auditors to the audit committee, the committee recommended that the board of directors include the audited consolidated financial statements in our annual report on Form 10-K for the fiscal year ended December 31, 2003.

The Members of the Audit Committee

| Henry C. Beinstein Robert J. Eide Richard J. Lampen |

Notwithstanding anything to the contrary set forth in our previous filings under the Securities Act or the Exchange Act that might incorporate future filings made by us under those statutes, the sections set forth above under the captions entitled "Compensation Committee Report on Executive Compensation," "Audit Committee Information and Report" and below under the caption entitled "Stock Price Performance Graph" will not be incorporated by reference in any of those prior filings or any future filings by us.

Executive Compensation

The following table shows the compensation paid or accrued by us to our chief executive officer and to our most highly compensated executive officers whose total 2003 compensation exceeded $100,000 (collectively, the "Named Executive Officers") for the calendar years 2003, 2002 and 2001. All compensation figures in this table and the notes thereto are in dollars.

| Name and Principal Position | Fiscal Period |

Annual Compensation | Long-Term Compensation |

All Other Compensation | ||||||||||||||||||

| Salary ($) | Bonus ($) | Options (#) | ||||||||||||||||||||

| Victor M. Rivas | 2003 | 500,000 | 500,000 | (1) | -0- | 2,254 | (2) | |||||||||||||||

| Former President and | 2002 | 500,000 | 595,678 | (3) | 300,000 | 3,044 | (2) | |||||||||||||||

| Chief Executive Officer | 2001 | 500,000 | (4) | 867,826 | (5) | 1,000,000 | 375,000 | (6) | ||||||||||||||

| Mark Zeitchick | 2003 | 90,000 | 307,981 | (7) | -0- | 79,580 | (2) | |||||||||||||||

| Former Executive Vice | 2002 | 90,000 | 378,055 | (7) | 250,000 | 32,357 | (2) | |||||||||||||||

| President | 2001 | 66,500 | 379,681 | (7) | -0- | 15,458 | (2) | |||||||||||||||

| Vincent A. Mangone | 2003 | 90,000 | 307,981 | (7) | -0- | 85,378 | (2) | |||||||||||||||

| Former Executive Vice | 2002 | 90,000 | 378,055 | (7) | 250,000 | 40,341 | (2) | |||||||||||||||

| President | 2001 | 66,500 | 379,681 | (7) | -0- | 10,752 | (2) | |||||||||||||||

| Salvatore Giardina | 2003 | 214,000 | 55,000 | (8) | 30,000 | -0- | ||||||||||||||||

| Vice President and Chief | 2002 | 214,000 | -0- | 35,000 | 70 | (9) | ||||||||||||||||

| Financial Officer | 2001 | 214,000 | 3,500 | (8) | -0- | 709 | (9) | |||||||||||||||

| (1) | Represents a $500,000 bonus paid by us. |

| (2) | Represents commissions earned from customer accounts for which the individual is a designated account representative. |

| (3) | Represents (i) a $500,000 bonus paid by us and (ii) a $95,678 bonus paid by us under our Incentive Plan. |

| (4) | Represents $173,973 of salary paid by Ladenburg prior to the consummation of the stock purchase agreement with New Valley, Berliner and Ladenburg on May 7, 2001 and $326,027 of salary paid thereafter by us. |

| (5) | Represents (i) a $173,973 bonus paid by Ladenburg, (ii) a $326,027 bonus paid by us pursuant to his employment agreement and (iii) a $367,826 bonus paid by us under our Incentive Plan. |

13

| (6) | Represents the portion of a fee paid by New Valley to Mr. Rivas which was reimbursed by Ladenburg for his services in connection with the closing of the stock purchase agreement with New Valley, Berliner and Ladenburg. |

| (7) | Represents a bonus paid to the individual under our Incentive Plan. |

| (8) | Represents a discretionary bonus received by the individual. |

| (9) | Represents residual earnings from stock options surrendered with respect to the 1995 merger of Ladenburg and New Valley. |

Compensation Arrangements for Executive Officers

Victor M. Rivas was formerly employed by us as our president and chief executive officer under an employment agreement with Ladenburg which would have expired in August 2004. On March 9, 2004, we entered into a severance, waiver and release agreement with Mr. Rivas. Under the severance agreement, effective March 31, 2004, Mr. Rivas retired from all of his positions with us and all of our subsidiaries including Ladenburg. Pursuant to the severance agreement, Mr. Rivas received (i) a lump sum payment of approximately $449,000 (representing various amounts owed to him under his existing employment agreement) and (ii) continued health benefits under his existing employment agreement until the earlier of his 65th birthday or until he is covered on a comparable basis by another plan.

In connection with Mr. Rivas' retirement, we entered into an employment agreement with Charles I. Johnston pursuant to which Mr. Johnston serves as our president and chief executive officer and as a member of our board of directors and as chairman and chief executive officer of Ladenburg effective as of April 1, 2004. The agreement continues indefinitely until terminated by either party in accordance with the agreement. Under the agreement, Mr. Johnston receives a base salary of $250,000 per year. Additionally, in connection with his commencing work for us, we paid him a bonus of $10,417 on April 1, 2004. We also issued Mr. Johnston options to purchase 2,500,000 shares of our common stock at a price of $0.75 per share, 1,000,000 of which are under our Equity Plan and 1,500,000 of which are outside the plan. The options vest based on Mr. Johnston's continued employment with us in five annual installments commencing on March 9, 2005 and expire on March 8, 2014. The options provide that if a "change of control" (as defined in the Employment Agreement) occurs, all options not yet vested will vest and become immediately exercisable. If Mr. Johnston is terminated by us for any reason other than for cause within the first year of the agreement, we are obligated to pay him $100,000 and 100,000 of his options will vest. Thereafter, we will be required to pay him a full year's base salary if we terminate his employment. The employment agreement also provides that Mr. Johnston will not compete with us or any of our subsidiaries in any company that is materially involved in the retail brokerage business for a period of one year from the date of his termination.

Salvatore Giardina is currently employed by us as our executive vice president and chief financial officer until April 1, 2005 under an employment agreement with Ladenburg. The employment agreement provides for an annual base salary of approximately $214,000 subject to periodic increases and discretionary bonuses as determined by our board of directors or our compensation committee. If Mr. Giardina is terminated by us for any reason other than for cause during the term of the agreement, we are obligated to pay him the remainder of his salary during the term of the agreement as a lump sum payment. The agreement provides that Mr. Giardina will not, for a period of one year from the date of his termination, solicit or induce any director, officer or employee of us or our subsidiaries to terminate such person's employment or to become employed by any other corporation or business.

Effective December 31, 2002, we entered into an amendment to Richard Rosenstock's employment agreement that provided for him to no longer be employed by us. However, he will continue to be employed by Ladenburg as a registered representative until December 31, 2005. Mr. Rosenstock, a member of our board of directors and our former vice chairman and chief operating officer, received $25,000 upon signing of the amendment and a monthly base salary of approximately $17,000 for the first year of the agreement and now receives a monthly base salary of $15,000 for the

14

duration of the agreement. Additionally, Mr. Rosenstock will receive 50% of all of his retail brokerage production for the term of the agreement and 15% of any compensation received by Ladenburg or any of its affiliates as a finders fee for any corporate finance transactions entered into within 18 months after the introduction by Mr. Rosenstock to Ladenburg. He is no longer entitled to participate in the Incentive Plan and Bonus Plan. The agreement provides that Mr. Rosenstock will not compete with us or our subsidiaries for a period of one year from the date of his termination, but allows him to deal with any of his prior or then existing customers or clients without any restriction. The signing bonus and base salary are considered a buy-out for accounting purposes, and accordingly, a total of $590,000 was accrued as of December 31, 2002 and included in operating expenses for 2002.

Messrs. Zeitchick and Mangone, our former executive vice presidents, were previously employed by us and Ladenburg Capital Management pursuant to five-year employment agreements dated August 24, 1999. Effective December 31, 2003, we entered into amendments to each of Messrs. Zeitchick's and Mangone's agreements that provided for them to terminate their employment with us as our executive vice presidents. The amendments provides for each of them to be employed with Ladenburg as a registered representative until August 31, 2004. Messrs. Zeitchick and Mangone will each receive a monthly base salary of approximately $4,000 for the duration of the agreement and be entitled to continue to participate in our Bonus Plan as well as receive an override (as defined in our Incentive Plan) at a rate of 0.25335%. They will also receive a 50% payout on all of their retail brokerage production in accordance with Ladenburg's standard procedures as well as 15% of any compensation received by Ladenburg or any of its affiliates as a finders fee for any corporate finance transactions entered into within 18 months after the introduction by them to Ladenburg. Additionally, each received $7,684 representing 20% of the amounts paid to Ladenburg Capital Fund Management, the general partner of the Ladenburg Focus Fund, as performance, management and other fees in connection with the fund during or relating to the year ended December 31, 2003. The agreements provide that Messrs. Zeitchick and Mangone will not compete with us or our subsidiaries for a period of one year from the date of their termination, but allows them to deal with any of their prior or then existing customers or clients without any restriction. The remaining salary payable under these amended employment agreements is considered a buy-out for accounting purposes, and accordingly, a total of $60,000 was accrued as of December 31, 2003 and included in operating expenses for 2003.

Compensation Arrangements for Directors

Directors who are employees of ours receive no cash compensation for serving as directors. Our non-employee directors receive annual fees of $15,000, payable in quarterly installments, for their services on our board of directors, and members of our audit committee and compensation committee each receive an additional annual fee of $10,000 and $5,000, respectively. In addition, each director receives five hundred dollars per meeting that he attends. Additionally, upon their election or re-election, as the case may be, we grant our non-employee directors ten-year options under our 1999 Performance Equity Plan to purchase 20,000 shares of our common stock at fair market value on the date of grant. All of our directors are reimbursed for their costs incurred in attending meetings of the board of directors or of the committees on which they serve.

Option Grants

The following table represents the stock options granted in the fiscal year ended December 31, 2003, to the Named Executive Officers.

| STOCK OPTION GRANTS IN 2003 | ||||||||||||||||||||||

| Name of Executive | Number of Securities Underlying Options Granted (#) |

Percent of Total Options Granted to Employees in Fiscal Year (%) |

Exercise Price of Options ($) |

Expiration Date |

Grant Date Present Value(1)($) |

|||||||||||||||||

| Salvatore Giardina | 30,000 | 2.6 | % | 0.45 | 12/16/13 | $ | 12,300 | |||||||||||||||

| (1) | The estimated present value at grant date of the options granted to such individual has been calculated using the Black-Scholes option pricing model, based upon the following assumptions: |

15

| volatility of 103.20%, a risk-free rate of 4.27%, an expected life of 10 years, a dividend rate of 0% and no forfeiture. The approach used in developing the assumptions upon which the Black-Scholes valuation was done is consistent with the requirements of Statement of Financial Accounting Standards No. 123, "Accounting for Stock-Based Compensation." |

The following table sets forth the fiscal year-end option values of outstanding options at December 31, 2003, and the dollar value of unexercised, in-the-money options for our Named Executive Officers. There were no stock options exercised by any of the Named Executive Officers in 2003.

| AGGREGATED FISCAL YEAR-END OPTION VALUES | ||||||||||||||||||

| Name | Number

of Securities Underlying Unexercised Options at Fiscal Year End: |

Dollar Value of Unexercised in-the-money Options at Fiscal Year End |

||||||||||||||||

| Exercisable (#) | Unexercisable (#) | Exercisable ($) | Unexercisable ($) | |||||||||||||||

| Victor M. Rivas | 766,666 | 533,334 | -0- | -0- | ||||||||||||||

| Mark Zeitchick | 183,333 | 166,667 | -0- | -0- | ||||||||||||||

| Vincent A. Mangone | 183,333 | 166,667 | -0- | -0- | ||||||||||||||

| Salvatore Giardina | 11,667 | 53,333 | -0- | -0- | ||||||||||||||

Annual Incentive Bonus Plan

On August 23, 1999, our shareholders adopted the Annual Incentive Bonus Plan, which is a performance-based compensation plan for our executive officers and other key employees. The plan is administered by our compensation committee and is intended to comply with the regulations issued under Section 162(m) of the Internal Revenue Code. Under this plan, bonuses are paid to participants selected by our compensation committee if performance targets established by our compensation committee are met within the specified performance periods. For the fiscal year ended December 31, 2003 and for the fiscal year ending December 31, 2004, our compensation committee determined that participating employees would share in a bonus pool equal to 25% of our net income before taxes and before the accrual of compensation payable under this plan provided that we achieve a 10% return on equity before taxes at the end of the fiscal year. The maximum award payable annually to any participant under this plan was limited to a percentage of the bonus pool created and was subject to the maximum limit of $5,000 for any person. The maximum award available to Victor M. Rivas under the Plan was limited to 32.5% of the Pool and the maximum award available to any other participant under the plan was limited to 22.5% of the Pool. No awards were made under the Bonus Plan for fiscal 2003 to Messrs. Rivas, Zeitchick and Mangone, the participants in the Bonus Plan for 2003. The compensation committee has selected Messrs. Zeitchick and Mangone to participate in the Bonus Plan for fiscal 2004.

Special Performance Incentive Plan

On August 23, 1999, our shareholders adopted our Special Performance Incentive Plan. The Incentive Plan is similar in nature to the Bonus Plan in seeking to provide performance-based compensation within the meaning of Section 162(m) of the Internal Revenue Code. Executive officers and key employees selected by our compensation committee may receive bonuses upon reaching performance targets established by our compensation committee within specific performance periods, which performance targets may be based upon one or more selected business criteria. For the fiscal year ended December 31, 2003 and for the fiscal year ending December 31, 2004, the compensation committee has determined that participants are entitled to receive an incentive award that is based on our total consolidated revenues provided that specified commission levels are achieved. Awards are payable monthly, based on the average monthly revenues to such date. However, final awards reflecting the performance for the last month of the fiscal period and the fiscal period overall are not paid until all financial results for the year are reconciled and the compensation committee has approved and certified that the established performance requirements have been achieved. The maximum award payable for any fiscal period to any participant is the lesser of $5,000,000 or a set

16

percentage for the individual participants as disclosed elsewhere in this report. Messrs. Zeitchick and Mangone received bonuses under the Incentive Plan for fiscal 2003 as disclosed in the Summary Compensation table above. The compensation committee has determined that Messrs. Zeitchick and Mangone will currently be entitled to participate in this plan for fiscal 2004.

1999 Performance Equity Plan

On August 23, 1999, our shareholders adopted the 1999 Performance Equity Plan covering 3,000,000 shares of our common stock, under which our officers, directors, key employees and consultants are eligible to receive incentive or non-qualified stock options, stock appreciation rights, restricted stock awards, deferred stock, stock reload options and other stock based awards. On May 7, 2001, our shareholders approved an amendment increasing the number of shares available for issuance under the plan to 5,500,000 shares. On November 6, 2002, our shareholders approved another amendment increasing the number of shares available for issuance under the plan to 10,000,000 shares. The Equity Plan will terminate when no further awards may be granted and awards granted are no longer outstanding, provided that incentive options may only be granted until May 26, 2009. The plan is intended to comply with the regulations issued under Section 162(m) of the Internal Revenue Code and is administered by our compensation committee. To the extent permitted under the provisions of the plan, the compensation committee has authority to determine the selection of participants, allotment of shares, price, and other conditions of awards.

Ladenburg Thalmann Financial Services Inc. Employee Stock Purchase Plan

In November 2002, our shareholders approved the "Ladenburg Thalmann Financial Services Inc. Employee Stock Purchase Plan," under which a total of 5,000,000 shares of common stock are available for issuance. Under this stock purchase plan, as currently administered by the compensation committee, all full-time employees may use a portion of their salary to acquire shares of our common stock. Option periods have been initially set at three months long and commence on January 1st, April 1st, July 1st and October 1st of each year and end on March 31st, June 30th, September 30th and December 31st of each year. On the first day of each option period, known as the "date of grant," each participating employee is automatically granted an option to purchase shares of our common stock to be automatically exercised on the last trading day of the three-month purchase period comprising an option period. The last trading day of an option period is known as an "exercise date." On the exercise date, the amounts withheld will be applied to purchase shares for the employee from us. The purchase price will be the lesser of 85% of the last sale price of our common stock on the date of grant or on the exercise date. The plan became effective November 6, 2002 and as of the date of this proxy statement, shares of common stock have been issued under it.

Equity Compensation Plan Information

The following table sets forth certain information at December 31, 2003 with respect to our equity compensation plans that provide for the issuance of options, warrants or rights to purchase our securities.

| Plan Category | Number of Securities to be Issued upon Exercise of Outstanding Options, Warrants and Rights |

Weighted-Average Exercise Price of Outstanding Options, Warrants and Rights |

Number of Securities Remaining Available for Future Issuance under Equity Compensation Plans (excluding securities reflected in the first column) |

|||||||||||

| Equity Compensation Plans Approved by Security Holders | 5,453,030 | $ | 1.76 | 4,546,970 | ||||||||||

| Equity Compensation Plans Not Approved by Security Holders | 200,000 | $ | 1.00 | -0- | ||||||||||

On August 31, 2001, New Valley and Frost-Nevada each loaned us $1,000,000. As consideration for the loans, we issued to each of them a five-year, immediately exercisable warrant to purchase

17

100,000 shares of our common stock at an exercise price of $1.00 per share. These two warrants are our only equity compensation "plans" not approved by our shareholders.

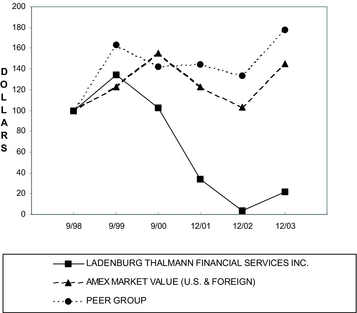

Stock Price Performance Graph

The graph below compares the cumulative total return of our common stock from January 1, 1998 through December 31, 2003 with the cumulative total return of companies comprising the Amex Composite Index (formerly the Amex Market Value Index) and a peer group selected by us based on comparative revenue. The graph plots the growth in value of an initial investment of $100 in each of our common stock, the Amex Composite Index and the peer groups selected by us over the indicated time periods, and assuming reinvestment of all dividends, if any, paid on our the securities. We have not paid any cash dividends and, therefore, the cumulative total return calculation for us is based solely upon stock price appreciation and not upon reinvestment of cash dividends. The stock price performance shown on the graph is not necessarily indicative of future price performance.

Our peer group is comprised of companies engaged in the same business that we are, each with revenues comparable to ours, and consists of the following companies: First Albany Companies, Inc., First Montauk Financial Corp., The John Nuveen Co., Kirlin Holding Corp., Crown Financial Group, Inc. (formerly M.H. Meyerson & Co., Inc.), Olympic Cascade Financial Corp., Paulson Capital Corp., Siebert Financial Corp. and Stifel Financial Corp.

COMPARISON OF 63 MONTH CUMULATIVE TOTAL

RETURN*

AMONG LADENBURG THALMANN FINANCIAL SERVICES

INC.,

THE AMEX MARKET VALUE (U.S. & FOREIGN) INDEX AND A PEER

GROUP

18

Section 16(a) Beneficial Ownership Reporting Compliance

Section 16(a) of the Securities Exchange Act of 1934, as amended, requires our officers, directors and persons who beneficially own more than ten percent of our common stock to file reports of ownership and changes in ownership with the SEC. These reporting persons are also required to furnish us with copies of all Section 16(a) forms they file. To our knowledge, based solely on our review of the copies of these forms furnished to us and representations that no other reports were required, all Section 16(a) reporting requirements were complied with during the fiscal year ending December 31, 2003.

Certain Relationships and Related Transactions

On May 7, 2001, we consummated the stock purchase agreement, as amended, with New Valley, Berliner Effektengesellschaft AG and Ladenburg in which we acquired all of the outstanding common stock of Ladenburg. This transaction and the subsequent Debt Conversion and repurchase of the senior convertible promissory note held by Berliner is described in greater detail under Proposal II, Debt Conversion, below.

Prior to the consummation of the acquisition of the outstanding common stock of Ladenburg, New Valley maintained office space at Ladenburg's principal offices. In connection with the consummation of the transaction, New Valley entered into a license agreement with Ladenburg in which New Valley will continue to occupy this space at no cost to New Valley. The license agreement is for one year and is automatically renewed for successive one-year periods unless terminated by New Valley. The space, which is not currently occupied by New Valley, has been subleased on a short-term basis by Ladenburg to an unaffiliated third party.

From June 2001 until October 2002, J. Bryant Kirkland III, the vice president, treasurer and chief financial officer of New Valley, served as our chief financial officer and New Valley did not allocate any expense to us for his services. In December 2002, we accrued compensation for Mr. Kirkland's services, in the amount of $100,000 which was paid in four quarterly installments of $25,000, commencing April 1, 2003.

On March 27, 2002, we borrowed $2,500,000 from New Valley. The loan, which bears interest at 1% above the prime rate, was due on the earlier of December 31, 2003 or the completion of one or more equity financings where we receive at least $5,000,000 in total proceeds. The terms of the loan restrict us from incurring or assuming any indebtedness that is not subordinated to the loan so long as the loan is outstanding. On July 16, 2002, we borrowed an additional $2,500,000 from New Valley on the same terms as the March 2002 loan. In November 2002, we completed the renegotiation of our clearing agreement with one of our clearing brokers whereby this clearing broker became our primary clearing broker, clearing substantially all of our business. As part of the new agreement with this clearing broker, an affiliate of the clearing broker loaned us an aggregate of $3,500,000 in December 2002. In connection with these loans, New Valley agreed to extend the maturity of its loans to December 31, 2006 and to subordinate its loans to the repayment of the loans made by the affiliate of our clearing broker.

On October 8, 2002, we borrowed an additional $2,000,000 from New Valley. The loan, which bore interest at 1% above the prime rate, matured on the earliest of December 31, 2002, the next business day after we received our federal income tax refund for the fiscal year ended September 30, 2002, and the next business day after we received a loan from an affiliate of our clearing broker in connection with the conversion of additional clearing business to this broker. This loan was repaid in December 2002 upon receipt of the loans made by the affiliate of our clearing broker.

We may from time to time borrow additional funds on a short-term basis from New Valley or from other parties, including our shareholders and clearing brokers, on terms which will be no less favorable than we could obtain from an unaffiliated third party in order to supplement the liquidity of our broker-dealer operations.

Howard Lorber is chairman of the board of directors of Hallman & Lorber Associates, Inc., a private consulting and actuarial firm, and related entities, which receive commissions from insurance policies written for us. These commissions amounted to approximately $48,000 in 2003.

19

Several members of the immediate families of our executive officers and directors are employed as registered representatives of Ladenburg. As such, they receive a percentage of commissions generated from customer accounts for which they are designated account representatives and are eligible to receive bonuses in the discretion of management. The arrangements we have with these individuals are similar to the arrangements we have with our other registered representatives. Richard Sonkin, the brother-in-law of Richard J. Rosenstock, received approximately $248,000 in compensation during 2003. Steven Zeitchick, the brother of Mark Zeitchick, received $329,000 in compensation during 2003. It is anticipated that each of these individuals will receive in excess of $60,000 in compensation from us in 2004.

20

PROPOSAL II

DEBT CONVERSION